From Hype to Reality: An Analytical Overview Of The Evolving Watch Industry

Watch prices are on a downward trajectory. Authorized dealers are increasingly stocking a variety of Rolex models and many other brands are available below retail on the secondary market. There's even talk of discounts from some authorized dealers.

What’s driving these changes and what do they mean for the industry? Let’s take a closer look.

Historical Context: 2019 - 2022

From 2019 to 2022, the watch market experienced unprecedented highs. Desirable models were not only scarce but also fetched prices well above retail on the secondary market. Flippers, gray market dealers and people touting watches as investments were what got spoken about. What's important though, is that 2019 to 2022 was the peak. This period marked the peak of the Rolex hype, which began around 2015 with the release of the steel ceramic Daytona. In 2018, manufacturers like Cartier even bought back stock to protect their brand. There were way too many watches in circulation. The model for watch manufacturers was to pump volumes and they would eventually end filling up display cases. But as we all know, this generated a massive glut of stock. Piles of watches were unsold and ADs rightly dumped them to the secondary market and this started negatively impacting brand perceptions. I mean, why would you pay full price when you could get more than 35% off on the secondary market?

The Impact of Covid-19

As the pandemic hit, production tightened and the economy fluctuated. With travel restrictions in place, consumers diverted their disposable income towards luxury watches, driving prices up and availability down. Now, as the market has stabilized, prices are coming down and previously hard-to-get models are becoming more accessible.

Current Availability

Many once-inaccessible models are now easier to find. Many unattainable watches from the past are now basically walk-ins or at the most command a waitlist of a month at max. Richemont's watch business saw contractions in late 2023 and the anticipated Christmas uptick didn’t occur. High-end brands, including Richard Mille, are seeing significant discounts on the secondary market.

A lot of high-end brands for a variety of reasons are nowhere near as desirable as they have been. Swatch in their Annual Report 2023 mentioned that they did very well for themselves in 2023, but nowhere near as well as 2022. They did note a slowdown towards the end of 2023. Also, while they're still optimistic for 2024 and beyond, there were statements indicating that the frenzy that they'd been once used to was over. LVMH also saw a slowdown in their watch business results and many other groups are also forecasting a massive slowdown.

Regional Variations and Consumer Behavior

The market outlook varies by region. European consumers are more pessimistic and cautious, leading to decreased purchases. Conversely, emerging markets like the Middle East and parts of Asia, especially India are experiencing growth, which is not completely unsurprising. These are regions where more millionaires are created every single day compared to anywhere else in the world.

According to Deloitte’s report titled “The Deloitte Swiss Watch Industry Study 2023,” and mentioned under the key findings, it states, “This was the first year India was mentioned so frequently as the next big growth market for the Swiss watch industry. By 2028, we predict that export sales of Swiss watches in India will reach over CHF 400 million. We think that India will be in the top 10 of Swiss export markets within a decade.”

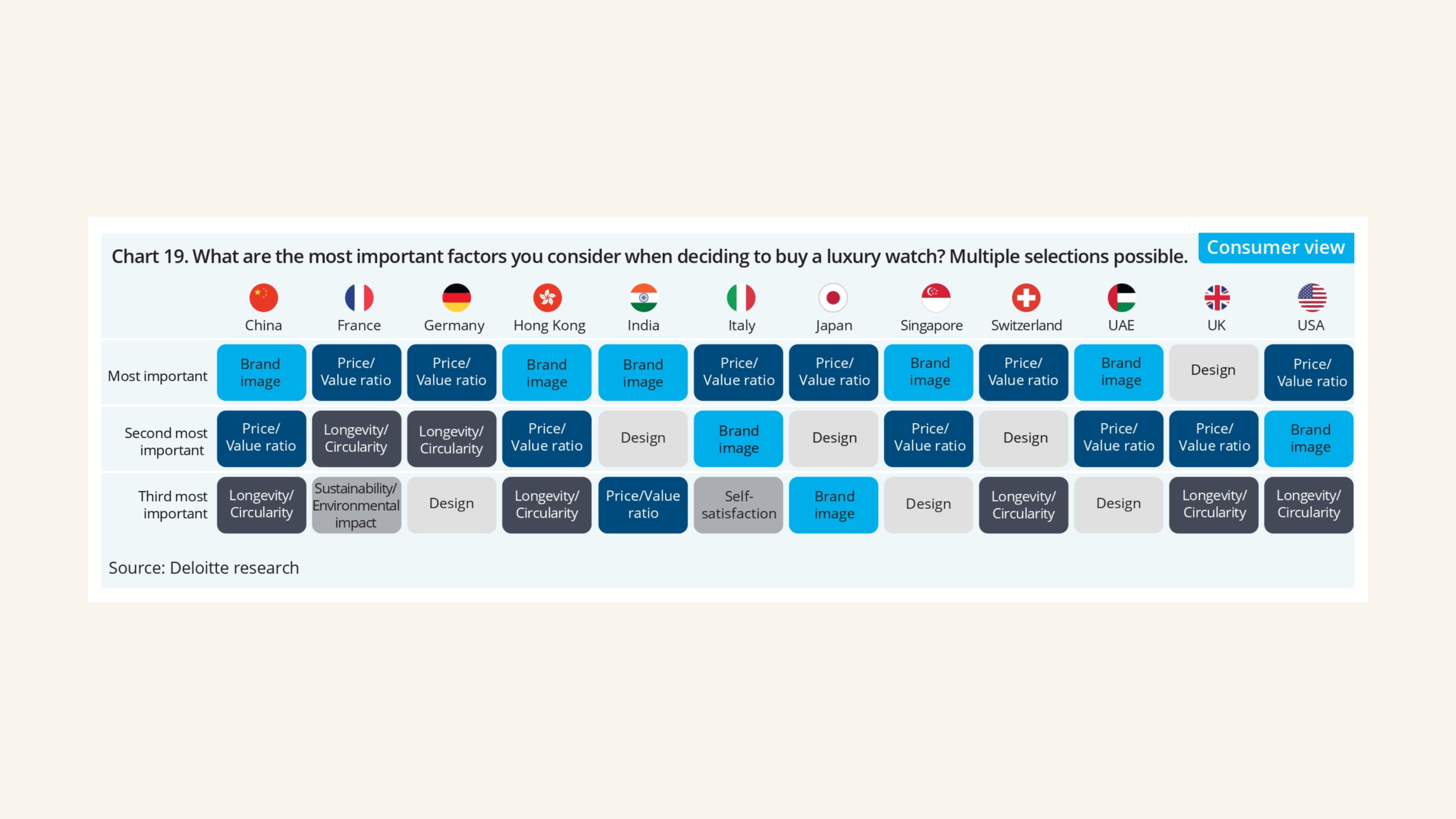

The report also states that consumers in the US and Europe are prioritizing value over brand, whereas buyers in India, the Emirates and China still place brand image first. This shift in consumer behavior is broadly reshaping the market landscape. It speaks to different buying behavior in general, but also to purchasing willingness. As the willingness to spend decreases, the preference for brand over value also diminishes.

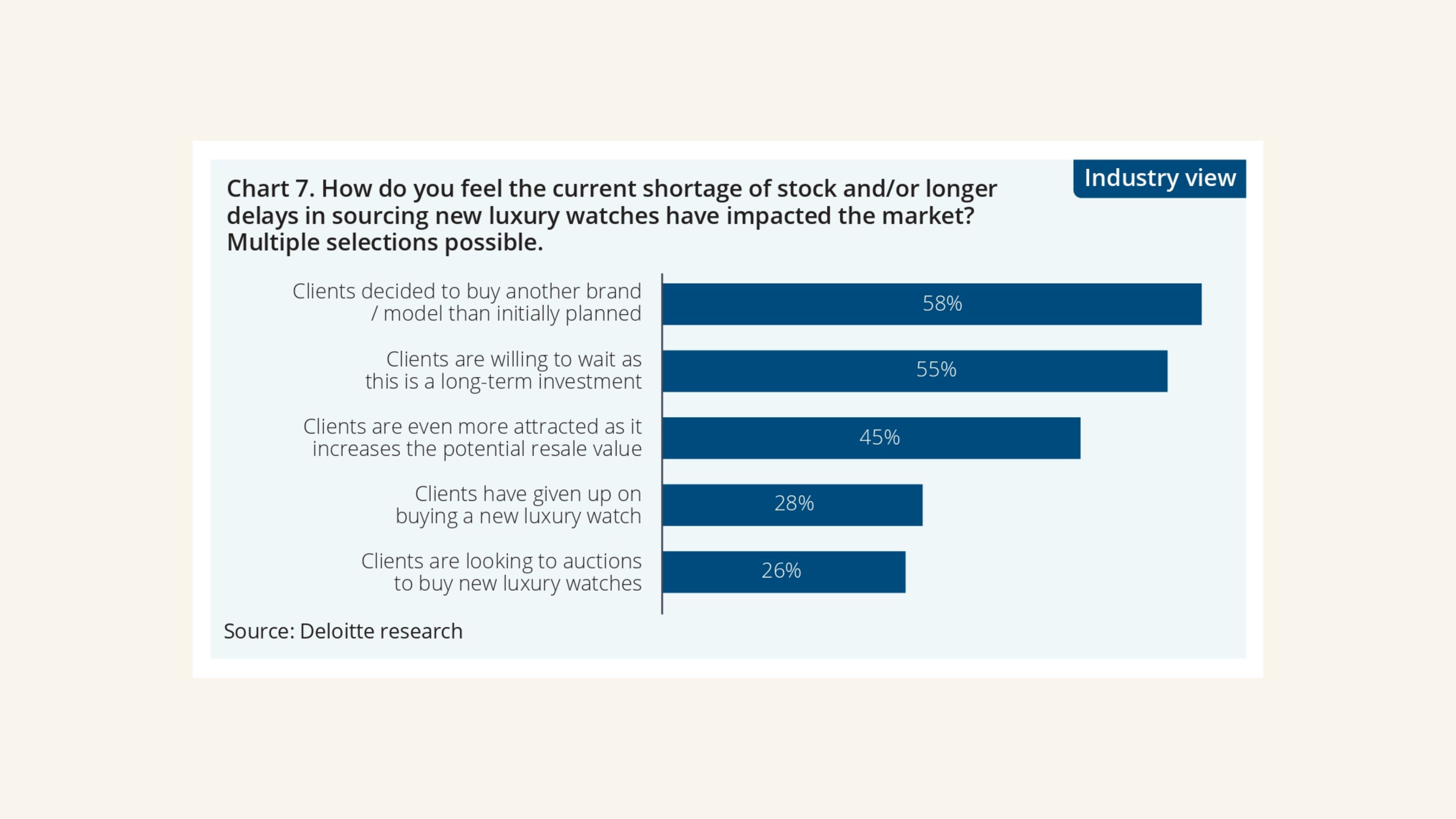

Another interesting data that the report captured was that in 2022, 20% of people who were on a waitlist gave up. In 2023, that number went up to 30%. Fewer people saw watches as a long-term investment and neither felt that the resale value of a watch was going to be higher because they had to wait for it. Even the brands seem to accept that people are tired of waiting for stock and more importantly, they'll either choose to buy from another brand or buy nothing at all. All in all, the fire days are over.

Market Predictions and Manufacturer Responses

Manufacturers are becoming more realistic about market conditions. While there is still some optimism for 2024, brands can no longer expect empty windows and must adjust to decreased demand. This shift is partly due to inflation, a slower economy and reduced disposable incomes. Moreover, the speculative investors and flippers who once drove prices up are now less active and manufacturers' price hikes during the pandemic are no longer sustainable. The decisions made in 2021-22 are impacting now in the first half of 2024. In short, consumers ran out of spare cash and got tired of waiting for the models they couldn't get. While we still get hyped for cool watches, we're just a little bit more hesitant, that bit more critical.

Strategic Adjustments for Brands

Brands aiming to move upscale will need to reconsider their strategies. Raising prices even by 15-20% in a slowing market is not viable. Instead, they must focus on maintaining value propositions and keeping price increases minimal to attract buyers. Limited edition releases, once a staple for driving demand, may need to be scaled back. Additionally, brands may reduce the variety of new releases to focus on safe bets, protecting market share rather than expanding it. Take an example of Rolex. Their price increases this year have been way humbler compared to what we've been used to.

Marketing and Consumer Shifts

Effective marketing has and will be crucial for brands to stand out. Despite economic pressures, those that invest in marketing will likely perform better. Swatch mentioned in their outlook for 2024 that they've realized that activities like the Swatch collabs drive massive sales. This could be a hint to even more such collabs in the future. As a matter of fact, if you don't scream in the crowd, nobody's going to notice you. But conversely, the moment the numbers go down, there's always a business tendency to cut back on the marketing, to protect the bottom line. So, brands going all in and strong on marketing are the ones that will perform better than the rest.

Value Attracts

Consumers are increasingly turning to smaller, niche brands that offer better value. Brands like Christopher Ward, Doxa, Maurice Lacroix, Oris, Frederique Constant and Tissot are gaining traction with high-quality and affordable models. This trend will push larger brands to innovate and justify their price premiums with superior specifications and features. An Omega Aqua Terra is a phenomenal watch, but there are options at half the price that some consumers are going to find compelling and they do pack in features like water-resistance, COSC certification and elaborate movement decorations. I don't think it's unreasonable to see a drift away from some of the big brands that have just gotten way too expensive for what you get.

Obviously, the manufacturers will react to that. So down the road, that drift will force brands like Omega, Breitling, Panerai and TAG Heuer to innovate. A lot of bigger brands have been resting on their laurels, living off of past successes. They really haven't done a lot in terms of movement innovations, bracelet designs and all that sort of stuff. The big brands will have to consider how they're going to justify their price premiums, in terms of specifications and finishing. Resting on their laurels isn’t an option anymore when it comes to specs.

The Future of High-End Brands

When it comes to high-end watch brands, we can expect a general contraction in demand. Brands such as Vacheron Constantin, will likely face more pressure compared to market leaders like Patek Philippe or Audemars Piguet. Similar to the enduring desirability of certain Rolex models, Patek Philippe will likely continue to attract buyers even as overall interest diminishes. Brands like Hublot, Richard Mille and F.P. Journe may see their clientele gravitate towards these more established high-end brands.

The Cycle Continues?

The next few years will be favorable for watch enthusiasts, with better availability and more reasonable prices. Although economic recovery will eventually drive-up demand and prices, the current period offers a unique opportunity for buyers. As history shows, the market will continue to cycle through periods of scarcity and abundance, with brands adapting to changing consumer behaviors and economic conditions. As the economy eventually rebounds, demand will rise again, repeating the cyclical nature of the market. For now, the balance has shifted in favor of the consumer, making it a great time to invest in luxury timepieces.