Swiss Watch Exports April 2026: What the Numbers Really Mean for the Industry

Headlines at a Glance

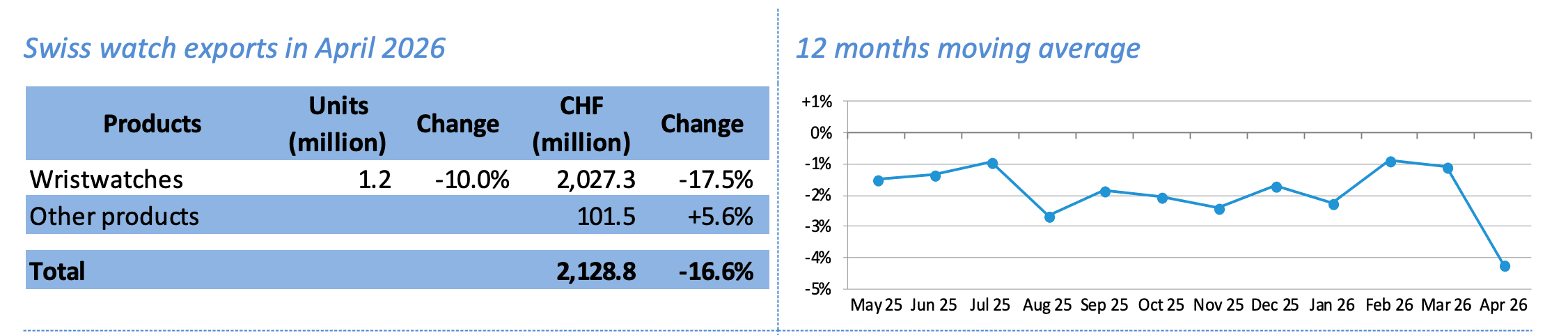

• Swiss watch exports fell 16.6% in April 2026, totalling CHF 2.13 billion

• Cumulative decline of 3.9% for January–April 2026

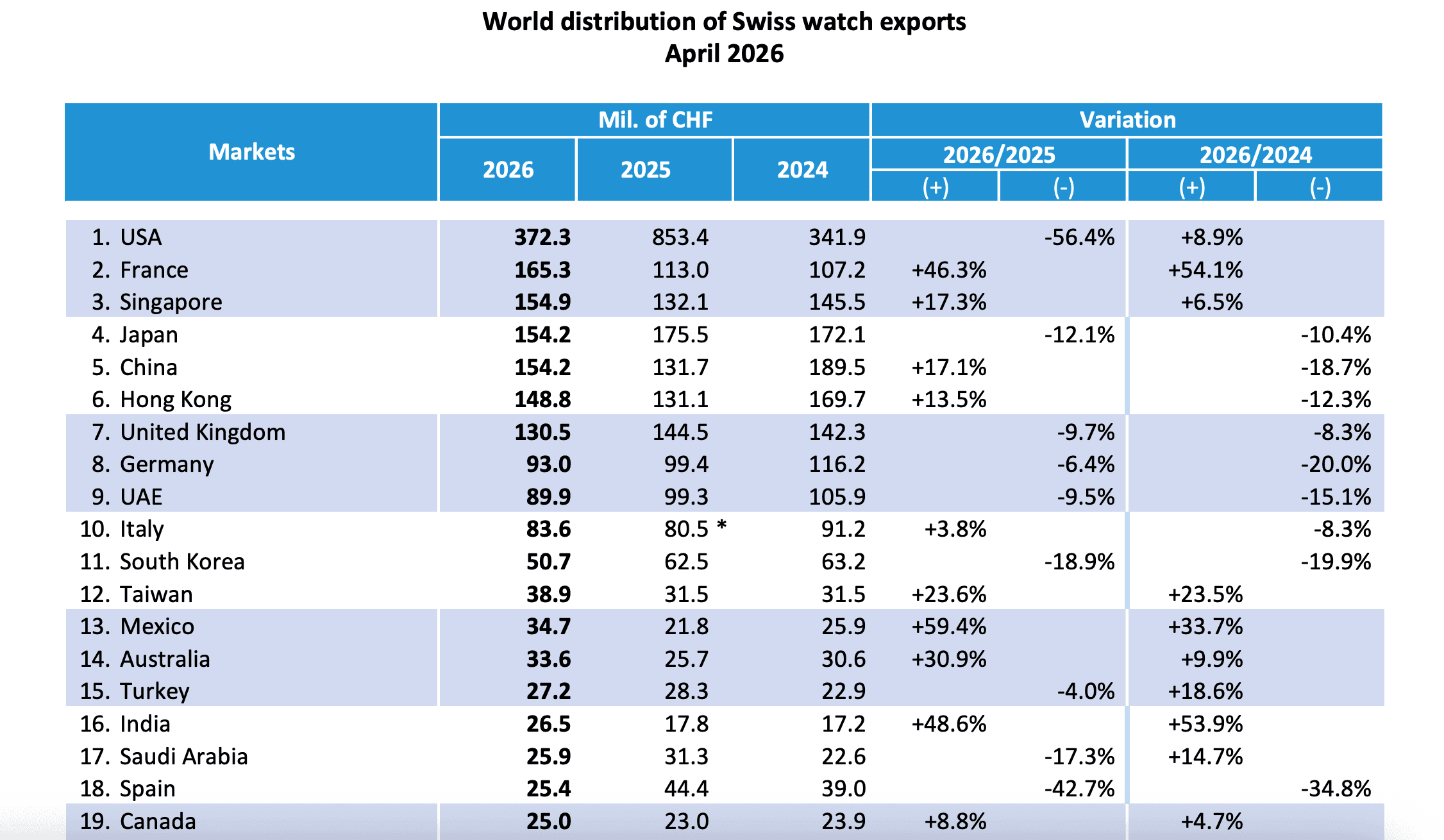

• The United States alone drove the majority of the drop - down 56.4% in April

• India is the standout growth story: +48.6% in April, +39% cumulative January–April year-on-year

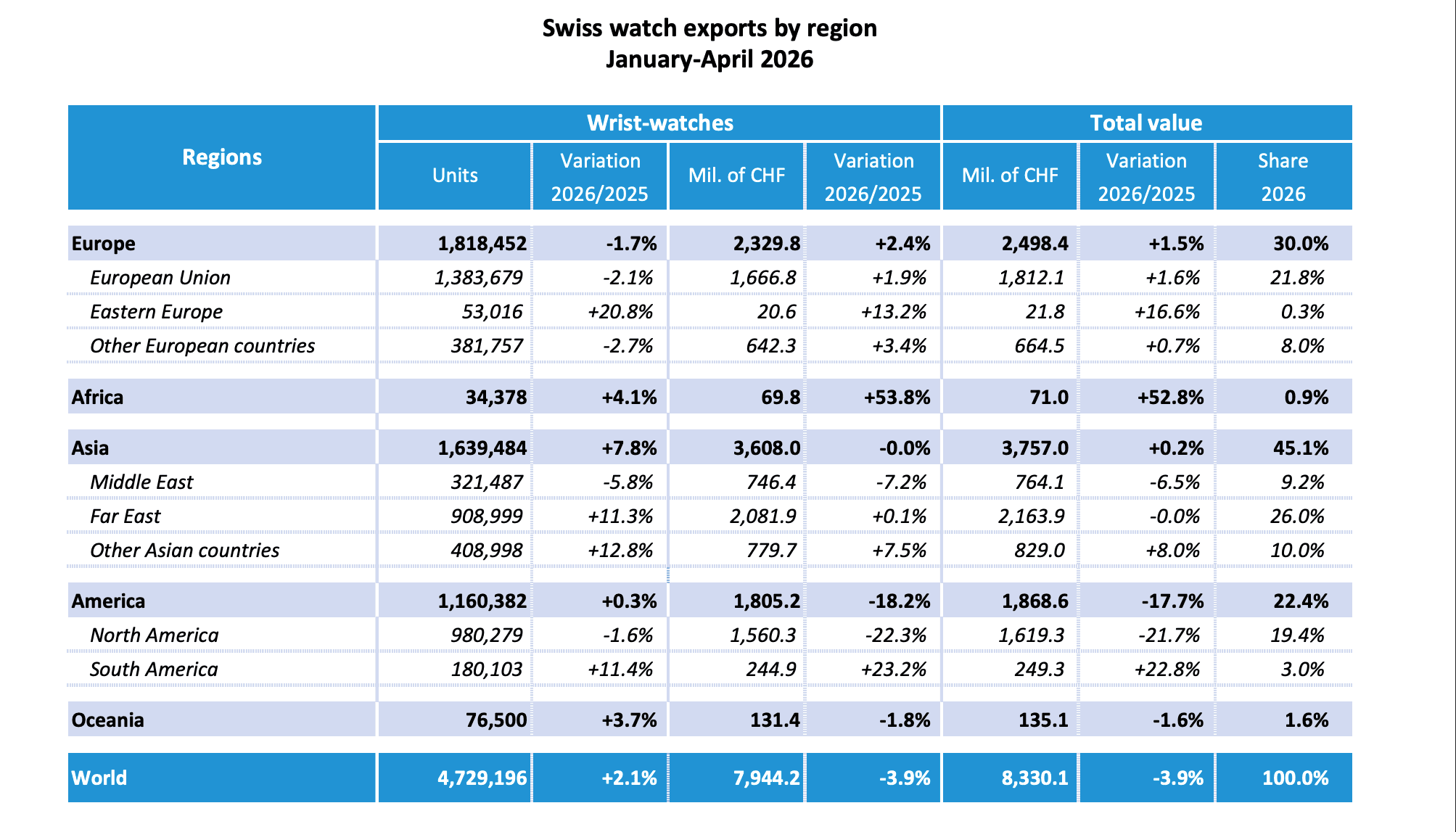

• Asia holds firm as the industry's largest region at 45% of total export value

The Big Picture: A Market Under Pressure - But Not in Crisis

Swiss watch exports are having a difficult 2026. The April numbers confirm what the 12-month moving average has been signalling since late 2025: the industry is in a correction, not a collapse. Total export value of CHF 2.13 billion in April represents a significant step back from the highs of recent years, and the cumulative CHF 8.33 billion for the first four months of the year is essentially flat compared to the same period in 2024, but down 3.9% versus 2025.

The critical context here is the United States distortion. April 2025 saw a sharp spike in US exports as brands and retailers front-loaded inventory ahead of anticipated tariff increases. That inflated base makes April 2026 look far worse than the underlying trend actually is. Strip out the US effect and the global picture is considerably more nuanced and in several key markets, genuinely encouraging.

The United States: A Distorted Picture

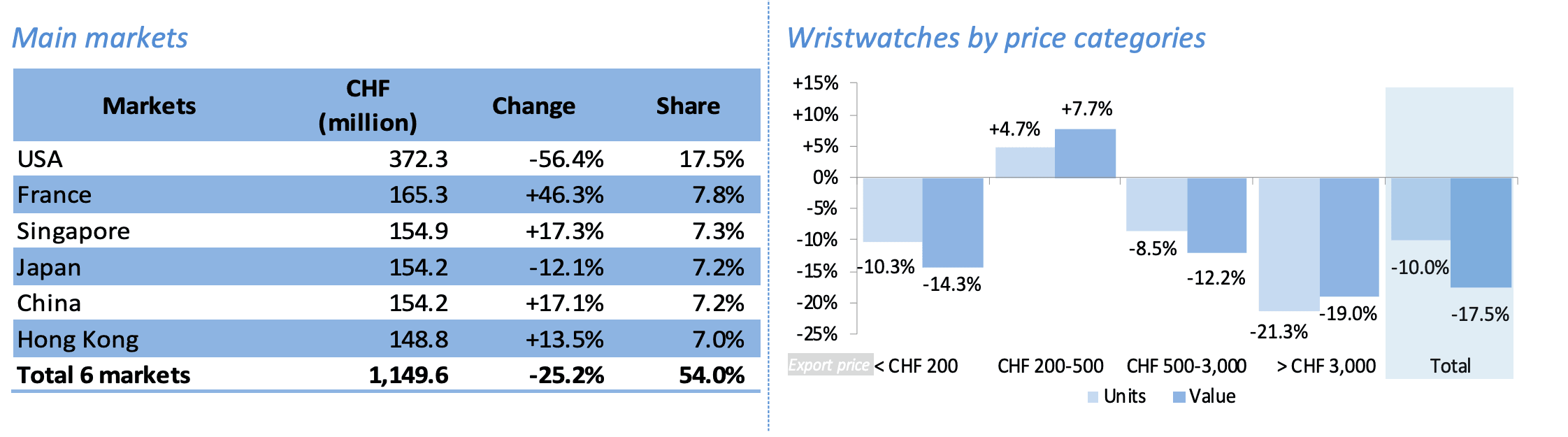

The US recorded a staggering 56.4% decline in April, falling to CHF 372.3 million. This is the single largest drag on the global number and demands context before conclusions are drawn. The drop is primarily a base effect in April 2025, brands rushed shipments to the US ahead of threatened tariff hikes, creating an artificially elevated comparison point. The FH itself notes that over the longer term, the US market has actually grown 8.9% compared with April 2024. For January–April 2026 cumulatively, the US remains the world's largest Swiss watch market at CHF 1,528.5 million, still ahead of France, Japan, Hong Kong, and China.

The takeaway: the US is not in structural decline. It experienced a one-off inventory correction that skewed the April data severely. Watch this space from Q3 onwards when the base effect normalises.

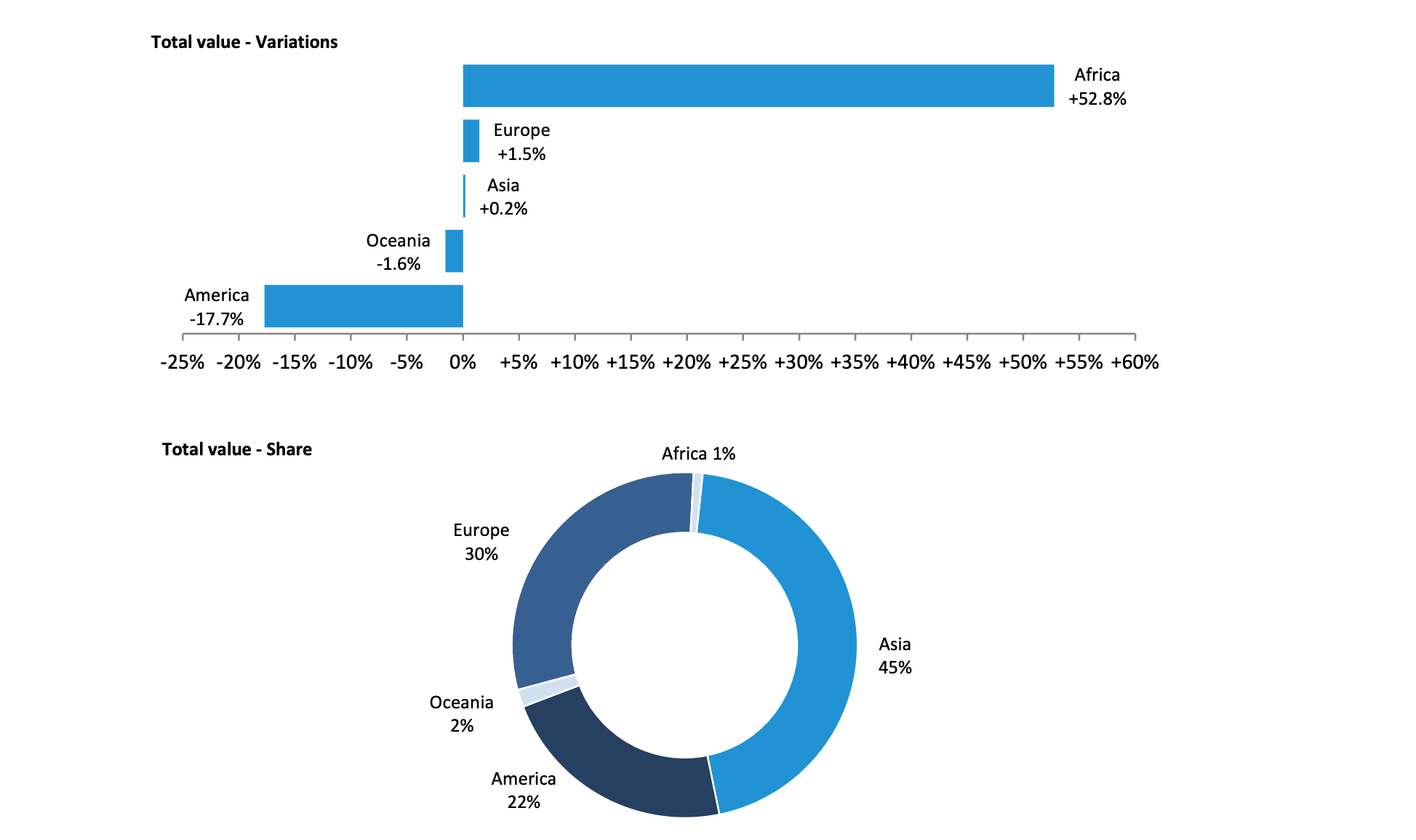

Asia: The Industry's Anchor

Asia accounts for 45% of total Swiss watch export value for January–April 2026 - the largest regional share by some distance, ahead of Europe at 30% and the Americas at 22%.

Within Asia, the picture is mixed:

China recorded CHF 574.6 million for the four-month period, up 3.5% versus 2025 though still down 22% compared to 2024's peak. The recovery is real but fragile. Consumer confidence in mainland China remains uneven, and the luxury sector continues to face headwinds from economic uncertainty and shifting spending patterns among younger consumers.

Hong Kong posted CHF 587 million, up 2.5% versus 2025, benefiting in part from a favourable base effect. It remains a critical re-export and collector hub.

Japan declined 3.8% to CHF 593.7 million, impacted by yen weakness and a slowdown in inbound tourist spending that had propped up retail figures in 2024 and early 2025.

Singapore grew 3.4% to CHF 543.6 million, continuing its role as Southeast Asia's most reliable luxury watch market.

The Middle East, historically a strong growth engine, fell 6.5% in total value, with the UAE down 9.5% and Saudi Arabia down 10.8%. This warrants monitoring, though Gulf markets have shown resilience historically and the declines may reflect specific retail inventory dynamics rather than demand erosion.

Europe: Quiet Stability and One Anomaly

Europe delivered +1.5% growth in total value for January–April 2026, a modest but meaningful result in a difficult global environment. The EU grew 1.6%, Eastern Europe surged 16.6% off a small base, and the UK declined 0.6%.

France is the statistical outlier - up 52.9% for the four-month period, making it the second-largest market globally at CHF 599.2 million. The FH explicitly flags that this does not reflect real consumer demand. France is a significant re-export hub; watches shipped to French distributors often end up across Europe and beyond. The number is a routing artefact, not a genuine indicator of French appetite. Germany fell 8.5%, continuing a softer trend that reflects broader consumer caution in Europe's largest economy.

Price Categories: The Premium Squeeze

The breakdown by price category reveals a concerning pattern for the high end of the market. Watches priced above CHF 3,000 at export the haute horlogerie and prestige segment fell 19% in value and 21.3% in units. This is the steepest decline across all categories and reflects both the US base effect (which disproportionately affects high-value pieces) and genuine softness at the top of the market globally.

The CHF 200–500 segment was the only category in growth, up 7.7% in value and 4.7% in units. This suggests that accessible luxury and entry-level Swiss watches are holding their own, a pattern consistent with broader luxury industry trends where the middle market is proving more resilient than the ultra-premium tier. By materials, precious metal watches took the hardest hit - down 24.3% in value and 26.1% in units. Steel models, which represent the industry's largest volume category at over 700,000 units, fell 18.1% in value and 10.6% in units. Only the "other metals" category grew, up 10% in value.

India: The Number Every Brand Should Be Talking About

Amid a report full of declines and caveats, India stands apart and the numbers tell two compelling stories depending on which lens you use. In April 2026 alone, India recorded CHF 26.5 million in Swiss watch exports - up +48.6% versus April 2025 and +53.9% versus April 2024. It ranked 16th globally for the month, ahead of Saudi Arabia, Spain, and Canada. Zooming out to the January–April 2026 cumulative picture, India recorded CHF 111.4 million, up +39.0% versus 2025 and +53.6% versus 2024. India now sits at 15th globally for the four-month period, having climbed rapidly from outside the top 20 just two years ago. To put the two-year trajectory in full context: India imported CHF 17.2 million of Swiss watches in April 2024. By April 2026, that monthly figure had grown to CHF 26.5 million - a 53.9% increase in 24 months. Cumulatively, the four-month total has risen from CHF 72.5 million in 2024 to CHF 111.4 million in 2026.

What This Means for the Industry: Five Conclusions

1. The US correction will pass. The April number is alarming on the surface but largely explained by inventory timing. The structural US market for Swiss watches remains large and growing on a two-year view. Brands should not overreact to a base-effect distortion.

2. Asia is the floor, not the ceiling. At 45% of global value and growing in unit terms (+7.8%), Asia remains the industry's most important region. China's partial recovery, Singapore's stability, and India's explosive growth collectively underpin the global market even as America wobbles.

3. The high end needs a new narrative. The 19% decline in watches above CHF 3,000 is the most structurally significant number in the report. Whether this reflects demand softness, a shift in collector preferences towards independents and micro-brands, or simply a post-pandemic correction in ultra-premium spending - brands at the top of the market need to work harder to justify their value proposition.

4. India is no longer a future market. It is a present one. +48.6% growth in April alone, +53.6% over two years, and rising collector sophistication mean that any brand without a clear India strategy is already behind. The window to establish positioning early is narrowing.

5. Distribution and partnership quality will determine winners. In a market growing as fast as India, the temptation is to move quickly with whoever is available. The brands that protect their equity through the right retail partners, the right events, the right market entry approach, will build durable positions. Those that don't will spend years rebuilding.

*Source : Federation of the Swiss watch industry FH