Steel Meets Gold: How Two-Tone Watches Are Powering Swiss Exports

2026 began on a rather worrisome note for Swiss Watch exports according to Frederation Of Swiss Watch Industry. If January delivered a warning shot, February offered reassurance, but not certainty. The first two months of 2026 reveal a Swiss watch industry navigating a fragile global landscape, where growth depends less on broad demand and more on the erratic performance of a few key markets and price tiers.

January: When Volume Rose but Value Fell

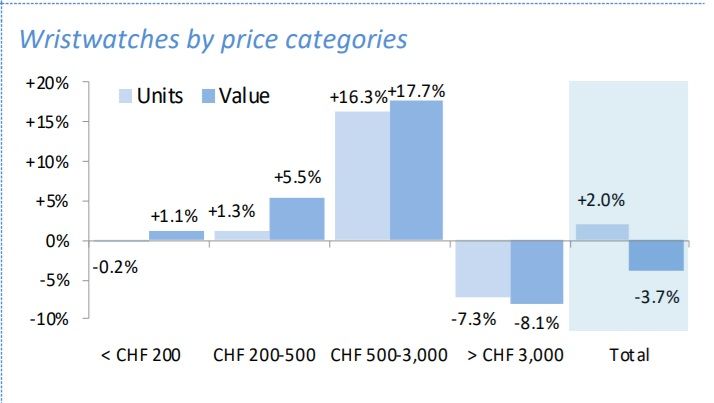

Swiss watch exports opened the year at CHF 1.92 billion, down 3.6% year-on-year a decline partly explained by one fewer working day, yet impossible to dismiss as purely technical. Wristwatch exports accounted for CHF 1.83 billion (-3.7%), while volumes actually rose 2.0% to 1.14 million units. This disconnect between units and value tells a crucial story: watches were moving, but not the ones that drive profit and prestige. The clearest weakness was at the top end. Exports of watches priced above CHF 3,000 fell 8.1%, dragging down overall performance despite strong growth of 17.7% in the CHF 500–3,000 segment. In other words, aspirational luxury remained active while the ultra-premium buyer hesitated.

Material data reinforces this shift:

- Precious-metal watches: CHF 618.8m (-14.0%), 27.5k units (-7.9%)

- Steel: CHF 627.3m (-4.5%), 659k units (-0.2%)

- Gold-steel: CHF 410.9m (+16.1%), 107.1k units (+45.1%)

- Other metals: CHF 103.7m (-1.3%), 78.7k units (-15.5%)

- Other materials: CHF 67.9m (+6.5%), 266.3k units (+2.9%)

Bimetal watches, long considered the pragmatic middle ground between luxury and affordability surged spectacularly, especially in volume. The message is clear: consumers are trading down, not exiting.

Geographically, the damage was amplified by the United States. The largest market fell to CHF 325.9 million (-14.0%), pulling the global total with it. Japan also declined (-7.5%), while Hong Kong (+2.6%) and mainland China (+5.0%) offered tentative signs of recovery. France stood out with a remarkable +36.8%, though such spikes often reflect re-exports rather than domestic consumption. The UAE rose 8.1%, reinforcing its role as a resilient luxury hub.

Other major declines painted a cautious global picture:

- Singapore: -14.3%

- United Kingdom: -6.3%

- Germany: -16.4%

January, in short, suggested a market still digesting the excesses of the post-pandemic boom.

February: A Rebound Powered by Confidence and Geography

Just one month later, the narrative shifted dramatically. February exports climbed to CHF 2.17 billion, up 9.2%, with wristwatches alone reaching CHF 2.07 billion (+10.0%). Volumes surged 14.0% to 1.27 million units, signalling genuine demand rather than inventory adjustment. Crucially, the high end returned to growth. All price segments expanded, with watches priced above CHF 500 driving the increase particularly the CHF 500–3,000 band, which grew at roughly double the pace of other segments.

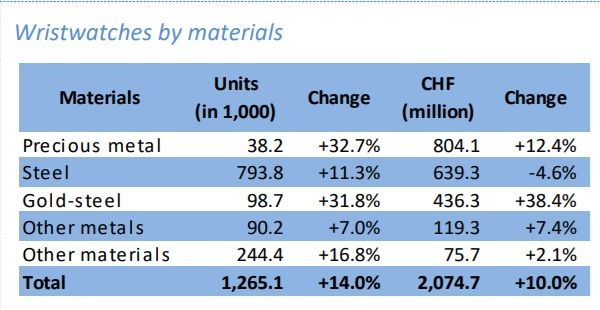

Material performance echoed this recovery:

- Precious-metal watches: CHF 804.1m (+12.4%), 38.2k units (+32.7%)

- Steel: CHF 639.3m (-4.6%), 793.8k units (+11.3%)

- Gold-steel: CHF 436.3m (+38.4%), 98.7k units (+31.8%)

- Other metals: CHF 119.3m (+7.4%), 90.2k units (+7.0%)

- Other materials: CHF 75.7m (+2.1%), 244.4k units (+16.8%)

Steel’s peculiar pattern rising volumes but falling value hints at a shift toward entry-level luxury steel models rather than flagship pieces. The real engine of February’s recovery, however, was geography. The United States swung violently from contraction to expansion, jumping to CHF 431.5 million (+26.8%) and reclaiming nearly one-fifth of global exports. Japan rebounded strongly to CHF 155.9 million (+23.7%), while France surged again to CHF 152.7 million (+57.1%), likely reflecting its role as a distribution hub.

India rose to 17th position accounting for CHF 52.2 million a jump from 26.2% compared to 2025. In 2025 the number stood at CHF 41.4 million and 2024 recorded CHF 34.3 million. This increase is significant as India strengthens its position as an emerging voice of authority in the global watch industry.

When it comes to watch movement exports, total Swiss exports fell 24.9% in the months of January-February 2026 as compared to January February 2025. Total units stood at 85,510 in 2025 as compared to 57,554 in 2026 during the same time period.

Other key markets delivered mixed signals:

- United Kingdom: CHF 142.3m (+10.0%)

- Singapore: CHF 135.7m (+5.1%)

- UAE: +5.1% (steady despite regional tensions)

- Hong Kong: -5.2%

- China: -11.0%

Greater China’s weakness remains the industry’s most persistent structural challenge. Once the engine of global growth, the region now oscillates between fragile recovery and renewed decline. Europe overall grew 7.2%, though unevenly: France and the UK advanced, while Germany (-3.5%) and Italy (-2.0%) slipped.

What It Means for the Swiss Watch Industry

Taken together, January and February expose an industry that is not shrinking but recalibrating. First, demand has not disappeared; it has stratified. Mid-luxury segments and bimetal watches are thriving, suggesting consumers still desire Swiss timepieces but are becoming more price-sensitive. Second, the United States is now the decisive market. Its swing from -14.0% to +26.8% within a month transformed the global picture. This concentration of dependence increases vulnerability to U.S. economic cycles and currency movements.

Third, Greater China remains an unresolved question. Continued declines in China (-11.0% in February) and Hong Kong (-5.2%) suggest that structural shifts from consumer confidence to travel patterns are still unfolding. Fourth, volume growth paired with uneven value growth points to changing consumption patterns. More watches are being shipped, but not always the most expensive ones. The era of effortless high-end expansion appears over, at least for now. Finally, the strong performance of France and other transit hubs underscores a subtle but important reality: global luxury distribution is increasingly complex, shaped by tourism flows, tax regimes, and re-export channels rather than purely domestic demand.

A Year Likely to Be Defined by Volatility

The opening months of 2026 do not signal crisis nor do they promise smooth growth. Instead, they reveal a market entering a more mature, unpredictable phase after years of extraordinary expansion. Swiss watchmaking remains resilient, anchored by brand power and global desirability. But the data suggests that future growth will depend less on broad-based demand and more on navigating regional cycles, pricing strategy, and shifting consumer psychology. If January was a reality check and February a relief rally, the rest of the year will determine whether the industry is stabilising or simply oscillating.