For nine years now, the Morgan Stanley/LuxeConsult “Swiss Watcher” has been the industry’s closest analogue to a financial briefing for an ecosystem that does everything it can to avoid publishing earnings. The 2025 edition makes something uncomfortably clear: the center of the Swiss watch business is not holding. The market has contracted for a second consecutive year, with exports down 1.7% in value terms and unit volumes more than halved versus the 2011 peak, yet the money has never been more concentrated at the very top.

A Brief Overview

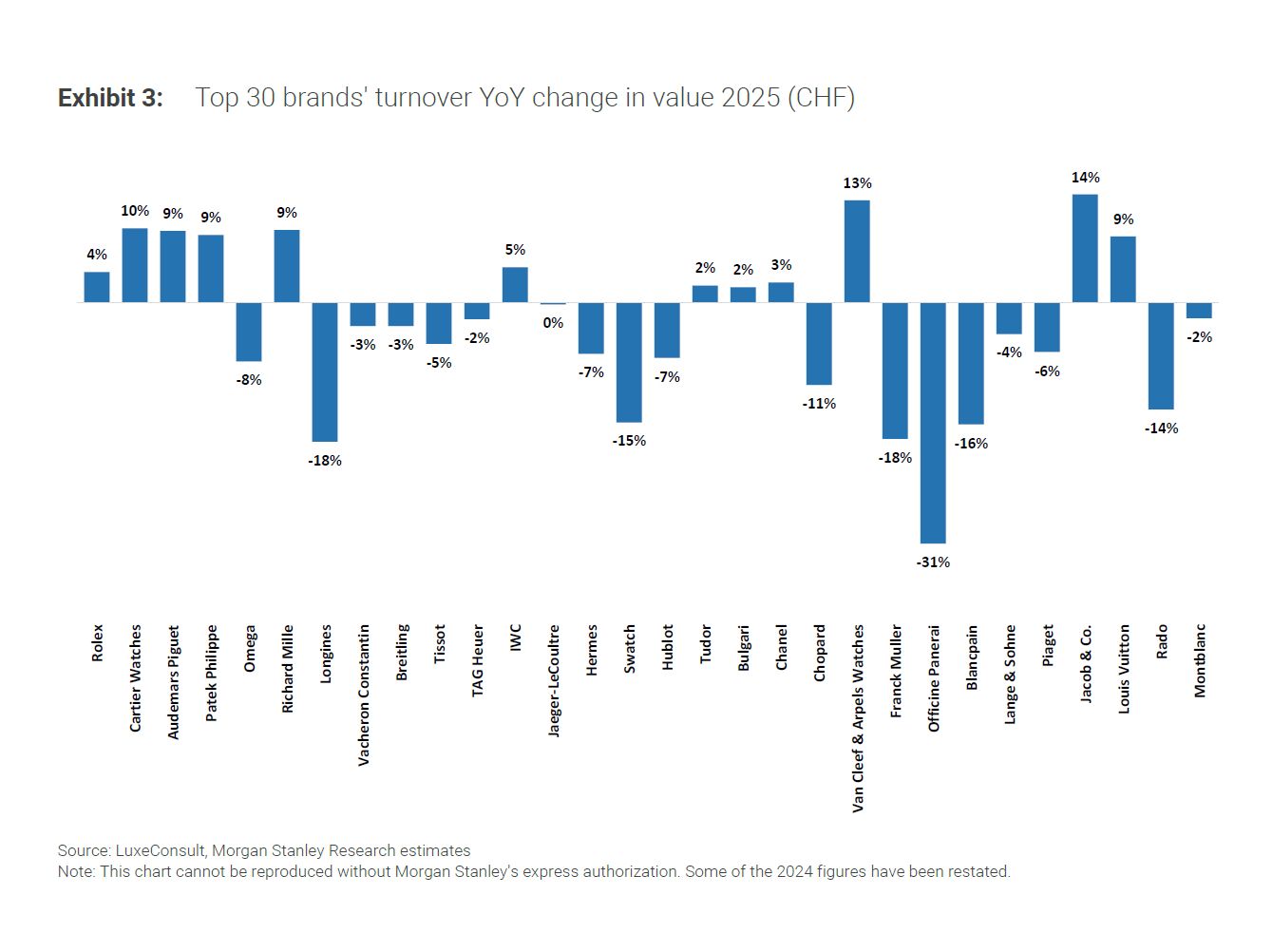

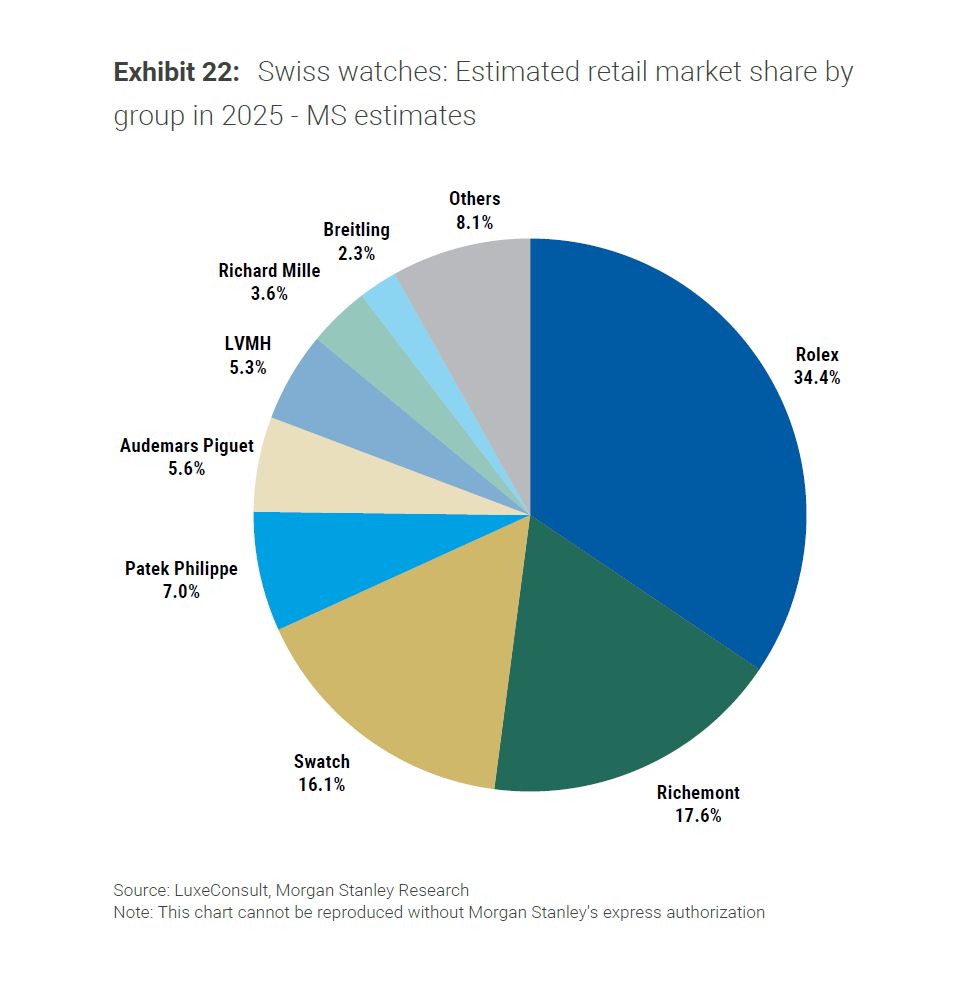

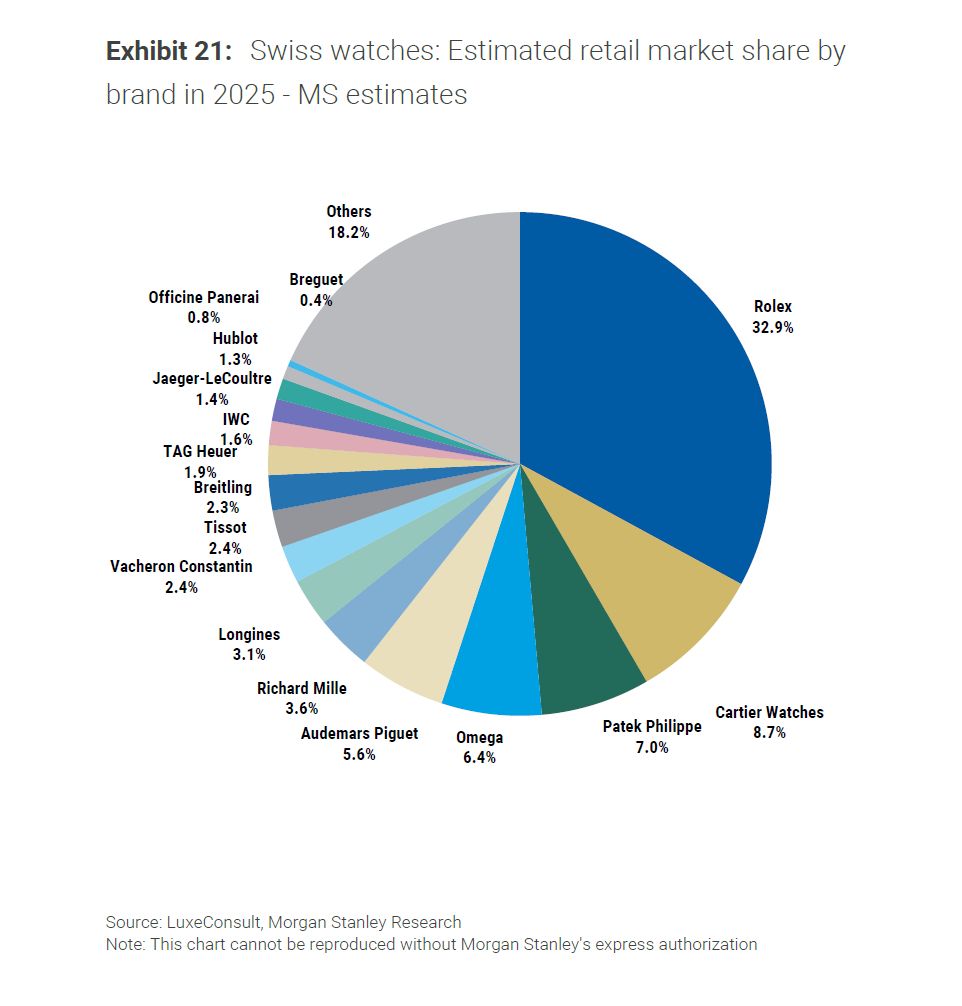

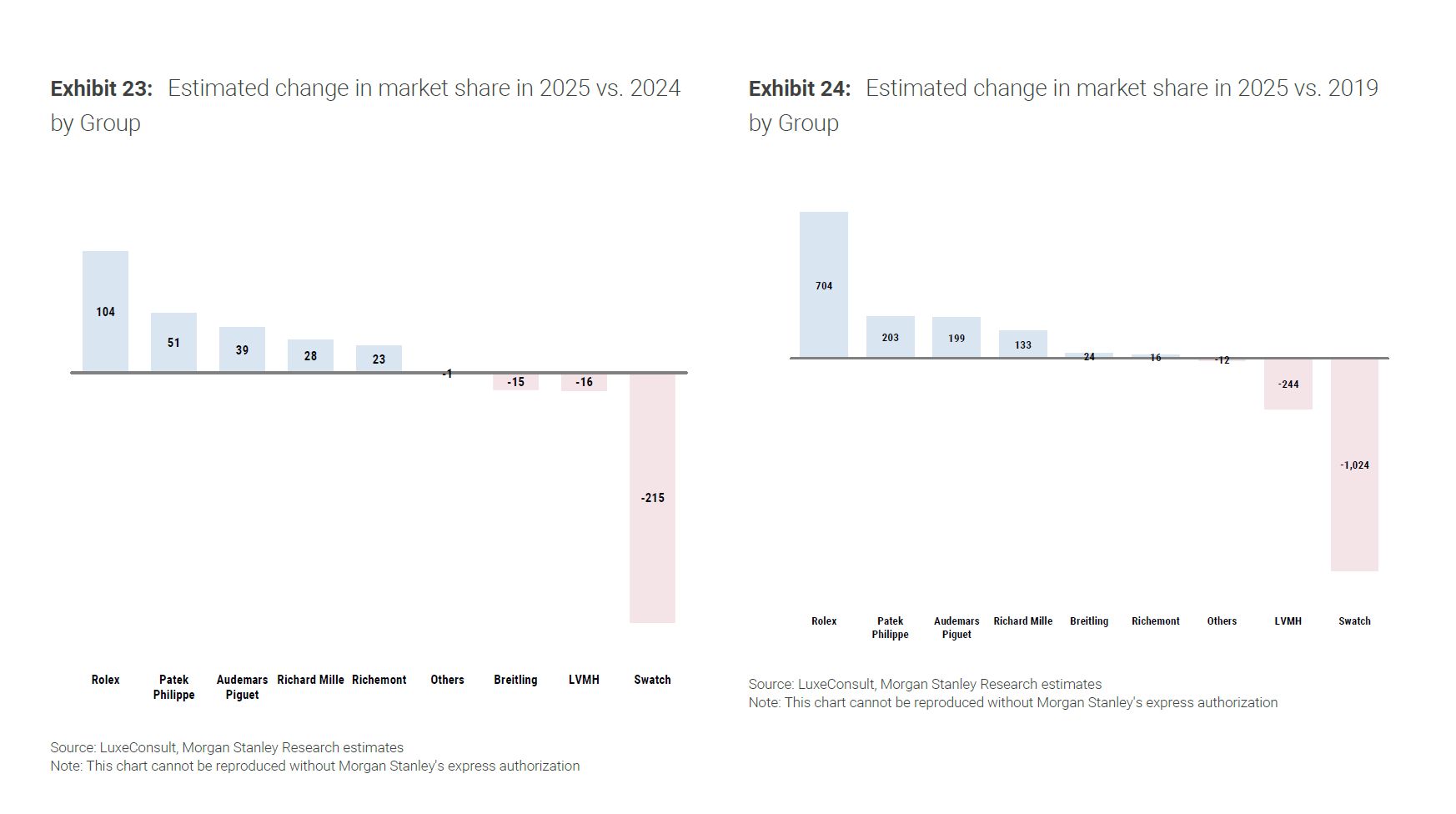

According to the report, the four leading brands now command over 50% of the entire Swiss watch market, with “The Big 4” - Rolex, Patek Philippe, Audemars Piguet and Richard Mille - structurally insulated from the turbulence buffeting almost everyone else. Rolex remains the preeminent leader, surpassing CHF 11 billion in wholesale sales while deliberately trimming volumes by an estimated 2% to around 1.1 million watches, the first back‑to‑back annual decline in production in over two decades, and a textbook exercise in managing scarcity to preserve long‑term desirability.

Below this summit, the landscape looks very different. Omega, once the perennial number two, now finds itself in fifth position by turnover, overtaken by Audemars Piguet and Patek Philippe, while Longines has slipped out of the so‑called “billionaires’ club” as sales dropped an estimated 18% to CHF 920 million. Swatch Group, long the volume backbone of Swiss watchmaking, has endured another year of meaningful share loss, even as it still accounts for roughly 60% of industry units at the entry and mid‑tiers. At the same time, a different narrative is playing out at the extremes: watches priced above CHF 50,000 now represent roughly 37% of export value and 89% of total growth, despite accounting for only about 1.4% of shipped pieces, while high‑end independents such as F.P. Journe, H. Moser & Cie., MB&F - and, notably, Christopher Ward at the more accessible end – continue to gain traction and even break into the Top 50.

The Ninth Annual Swiss Watcher is a sharp, data‑driven snapshot of a market polarising in real time, where a handful of brands write most of the P&L, the “middle class” is being squeezed from both sides, and the most dynamic stories are increasingly found at the very top and very edges of the price spectrum.

A Market That Shrank, And Concentrated

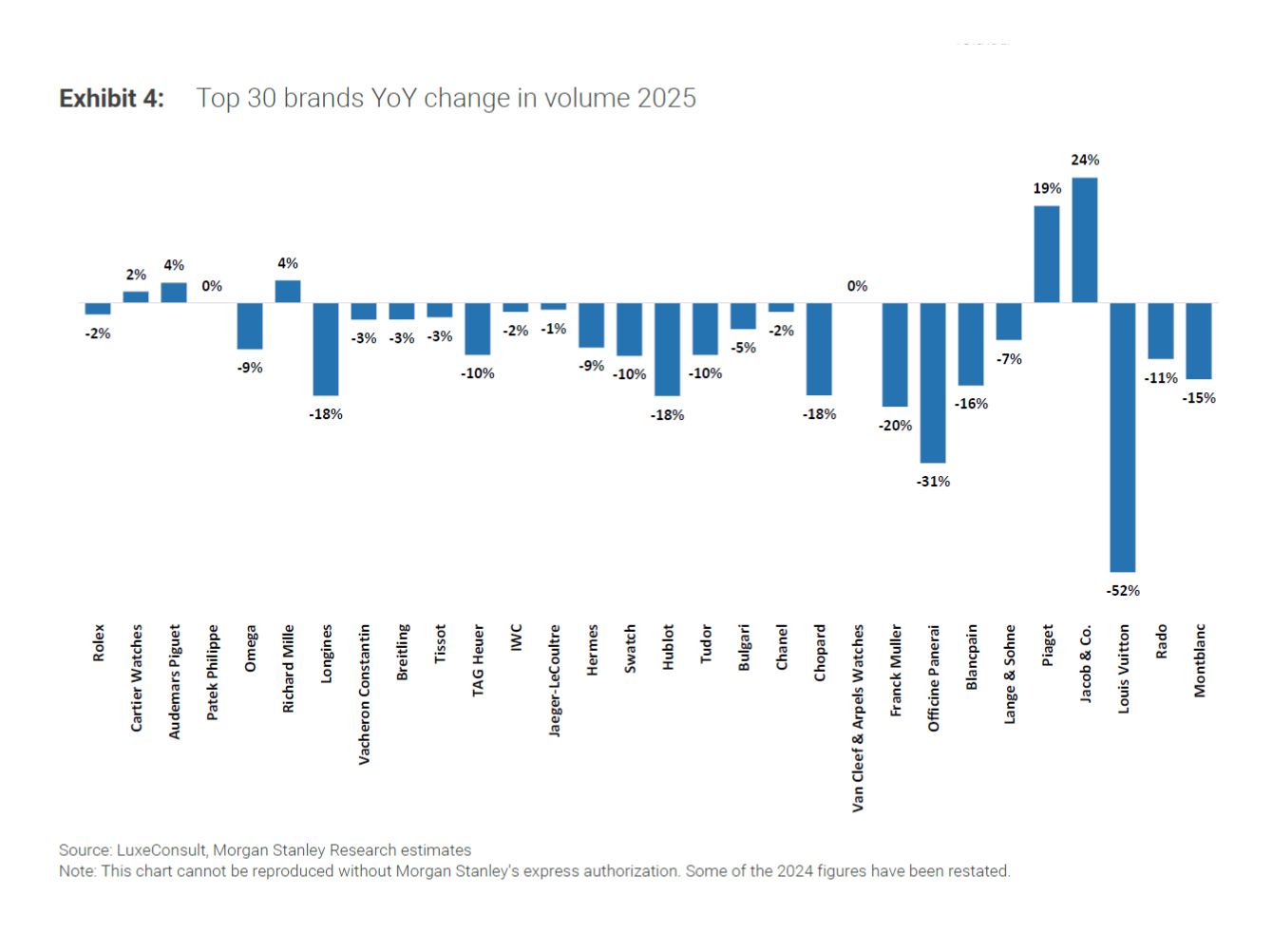

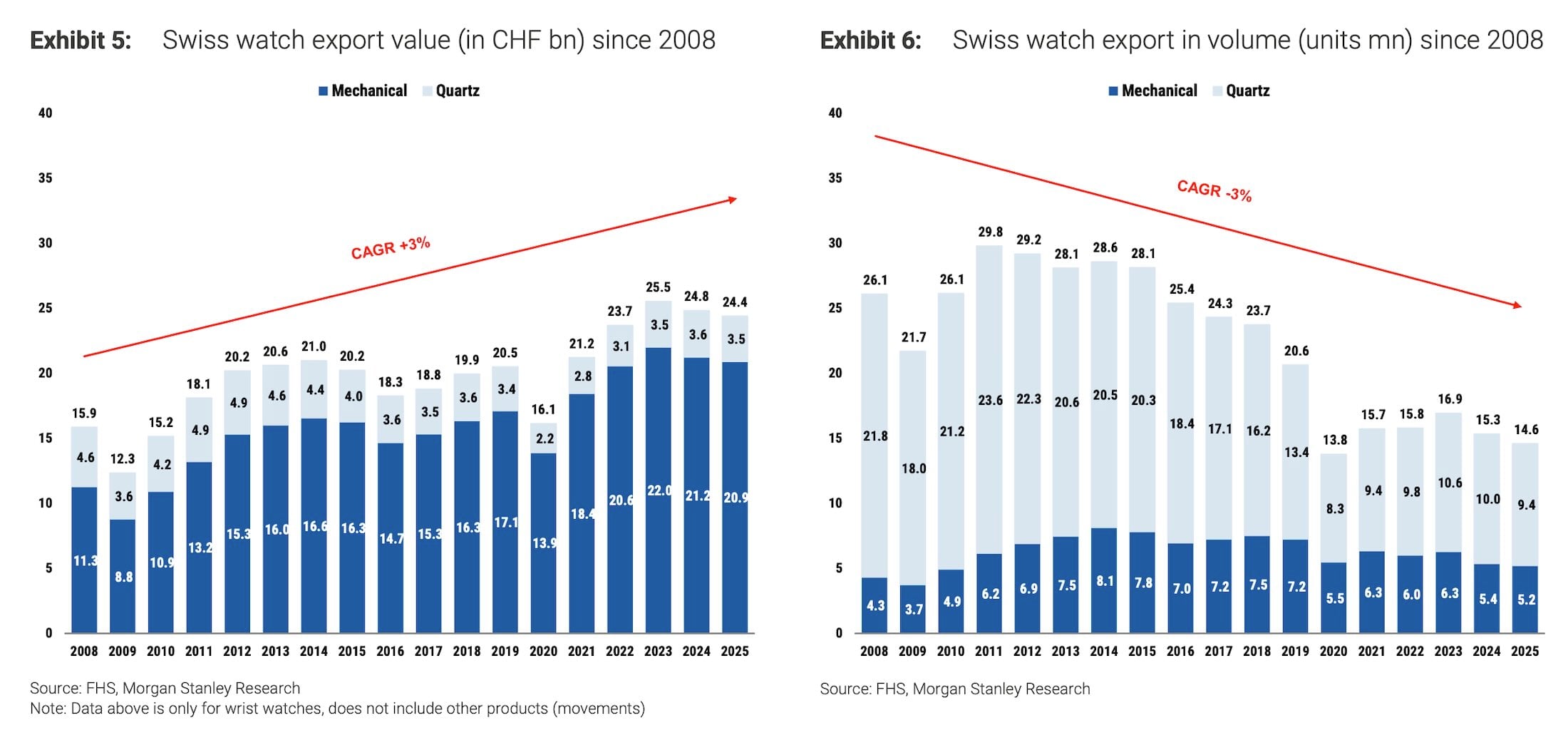

In 2025 the Swiss watch market contracted for the second consecutive year, with Swiss wristwatch exports down 1.7% in value to CHF 24.4 billion, even as the estimated global retail value of Swiss watches (ex‑VAT) remained a formidable CHF 49 billion. Volumes fell more sharply, down 4.8% to 14.6 million units, a multi‑decade low and barely half the 29.8 million units exported in 2011, underscoring how thoroughly Swiss watchmaking has become a value - not volume - business.

Premiumization accelerated: watches above CHF 50,000 represented 37% of export value in 2025 (up from 33.5% in 2024) yet accounted for only 1.4% of volumes, driving 89% of incremental value. At the other end of the spectrum, the Swatch Group’s mass and mid‑range portfolio still moves roughly 8.8 million watches, around 60% of Swiss volume, but its value share continues to erode.

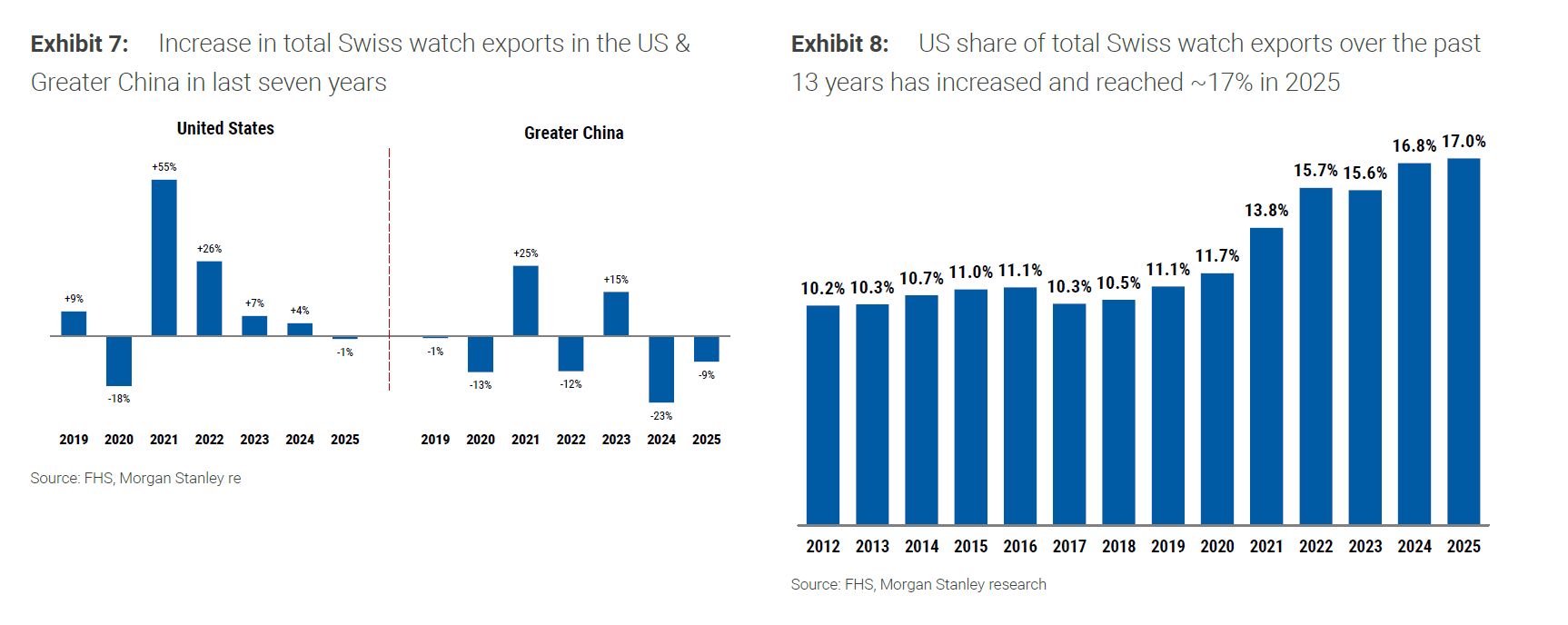

Geographically, the story is one of diverging trajectories. The United States remained the largest export market, absorbing about 17% of Swiss watch exports versus roughly 10% in 2012, even after a slight 1% decline in 2025. Greater China, by contrast, declined 9% in value and 13% in volume in 2025, leaving exports to the region about 40% below 2012 levels and reducing its share of exports to 14.1%. Brands structurally over‑indexed to Chinese demand - Longines, Tissot, Tudor and others - paid dearly for that exposure.

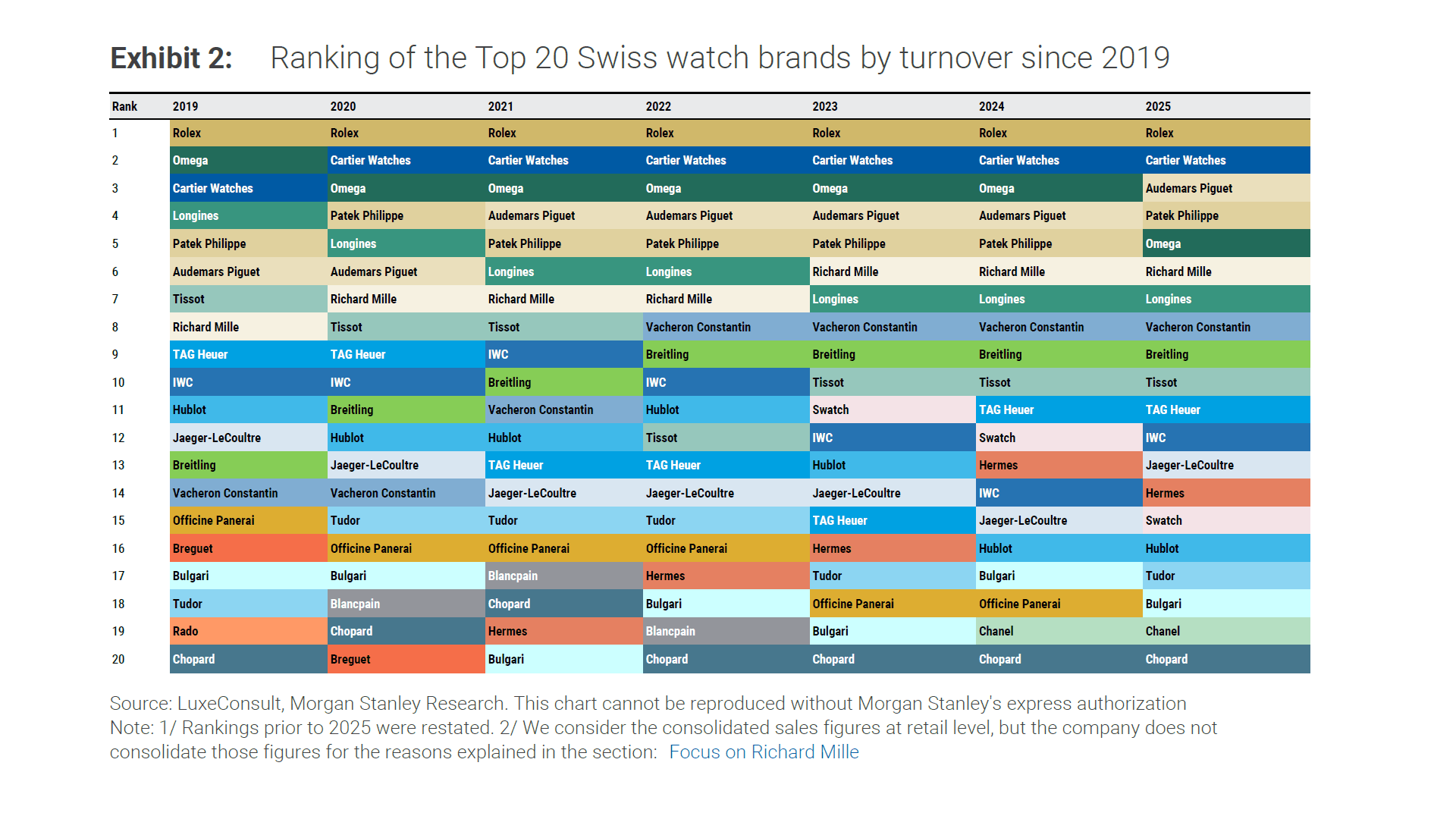

The Top 50, By The Numbers

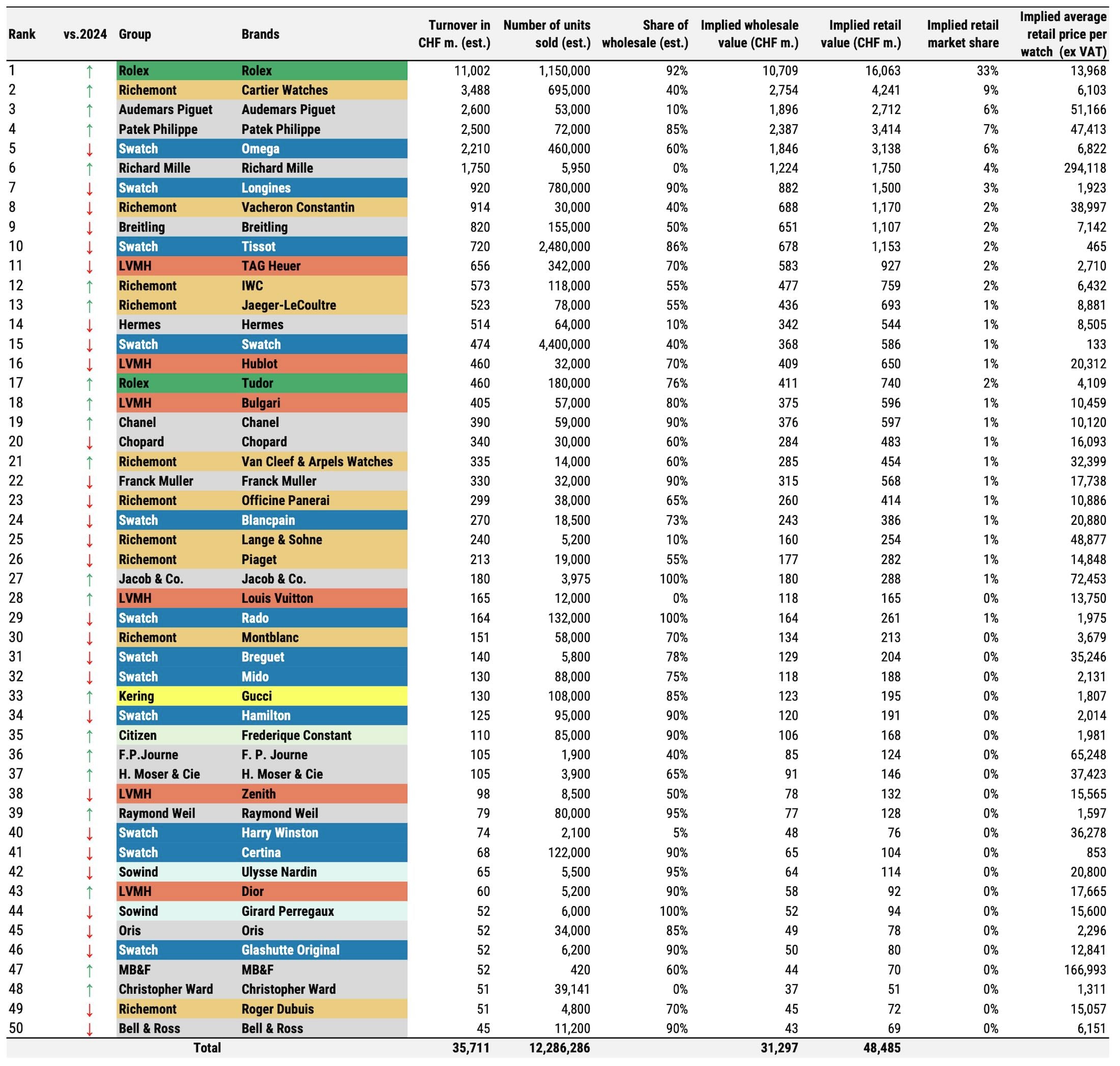

LuxeConsult and Morgan Stanley estimate that, out of roughly 450 Swiss brands, only six crossed CHF 1 billion in turnover at the wholesale level in 2025: Rolex, Cartier, Audemars Piguet, Patek Philippe, Omega and Richard Mille. Longines, hurt by China and aggressive past price hikes, fell out of this “Billionaires Club”, with sales down 18% to CHF 920 million, its first sub‑billion year in over a decade.

At the group level, the concentration is even starker. Rolex Group (Rolex + Tudor), Richemont, Swatch Group and Patek Philippe together control more than three‑quarters of Swiss watch retail sales by value. The four largest privately owned brands - Rolex, Patek Philippe, Audemars Piguet and Richard Mille, command 49.1% of the entire Swiss watch market by value, up 220 bps year‑on‑year and 1,240 bps versus 2019.

Top Brands And Market Share 2025

The full Top‑50 table in the Ninth Swiss Watchers report details turnover, unit volumes, wholesale and retail value, and implied ASP for each brand, collectively these 50 account for roughly CHF 48.5 billion of retail sales across some 12.3 million watches.

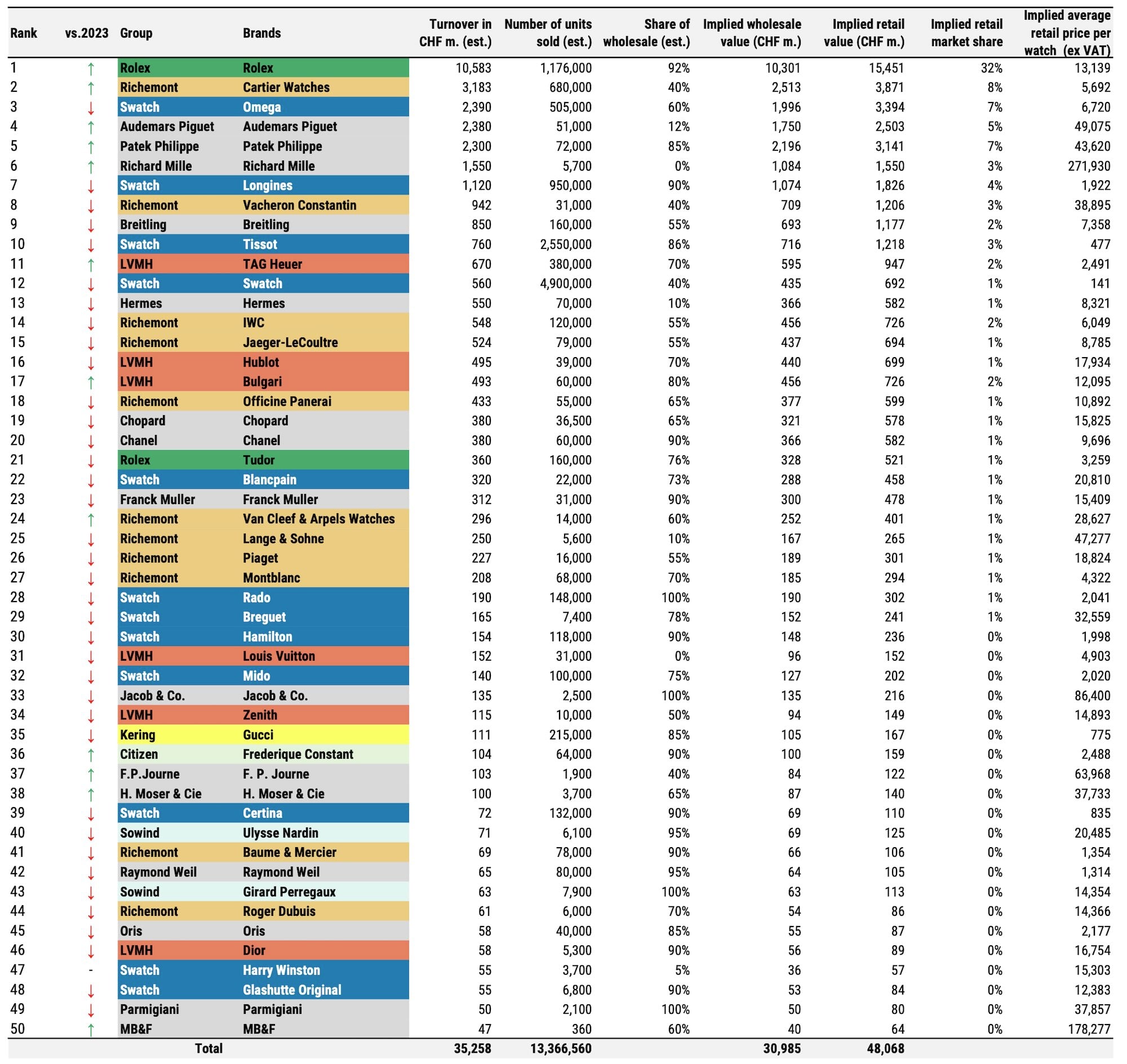

Here’s the 2024 table for comparison:

Here’s a table listing the Top 10 performing brands and the key takeaways for 2025:

Rank | Brand | Estimated Retail Market Share 2025 | Key 2025 Notes (ASP: Average Selling Price) |

1 | Rolex | 32.9% | Sales ~CHF 11.0 bn (+4%); volumes ~1.15m (‑2%); ASP ~CHF 14,000 (+6%). |

2 | Cartier Watches | 8.7% | Sales ~CHF 3.5 bn (+10%); ~695k units (+2%); ASP ~CHF 6,100. |

3 | Patek Philippe | 7.0% | Sales ~CHF 2.5 bn (+9%); ~72k units; ASP ~CHF 47,400. |

4 | Omega | 6.4% | Sales ~CHF 2.21 bn (‑8%); ~460k units (‑9%); ASP ~CHF 6,820. |

5 | Audemars Piguet | 5.6% | Sales ~CHF 2.6 bn (+9%); ~53k units (+4%); ASP ~CHF 51,166. |

6 | Richard Mille | 3.6% | Sales ~CHF 1.75 bn (+9%); ~5,950 units (+4%); ASP ~CHF 294,000. |

7 | Longines | 3.1% | Sales ~CHF 920m (‑18%); ~780k units (‑18%); ASP ~CHF 1,923. |

8 | Vacheron Constantin | 2.4% | Sales ~CHF 914m; ~30k units. |

9 | Tissot | 2.4% | Sales ~CHF 720m (‑5%); ~2.48m units; ASP ~CHF 465. |

10 | Breitling | 2.3% | Sales ~CHF 820m (‑3% reported); ~155k units; ASP ~CHF 7,142. |

- | “Others” (all other brands) | 18.2% | The remaining 430+ brands share less than a fifth of the value. |

If 2025 confirmed anything, it is that the profit pool belongs overwhelmingly to a tiny set of privately controlled houses. The four private giants: Rolex, Patek Philippe, Audemars Piguet, Richard Mille, generated an estimated CHF 18.3 billion in sales and captured 76% of the Swiss watch industry’s operating profit pool, with aggregate margins around 33%. Listed players (Richemont, Swatch, LVMH) together held 41% of sales but only 18% of profits, with an average margin in the low‑teens.

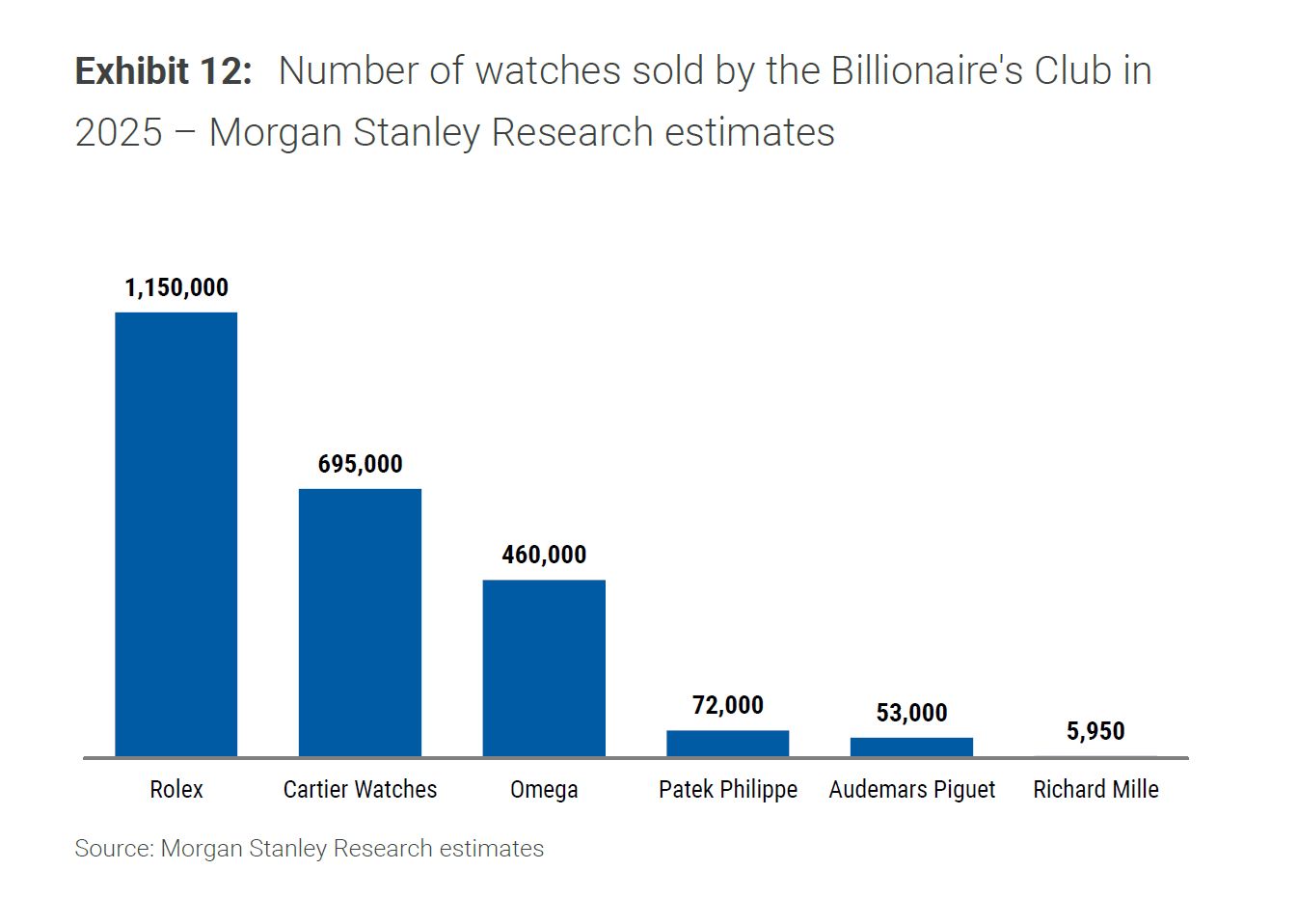

Rolex alone is estimated at about CHF 11.0 billion wholesale (CHF 16.1 billion implied retail), with ASP up roughly 50% since 2019 and volumes intentionally trimmed by about 2% in 2025 to an estimated 1.15 million units. That supply discipline allowed Rolex to gain 90 bps of market share in 2025, reaching 32.9% of Swiss watch value - and about 34.4% when Tudor’s CHF 460 million and ~180,000 units are included.

Rolex - Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2025 | 11,002 | 1,150,000 | 33% |

2024 | 10,583 | 1,176,000 | 32% |

Tudor - Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2025 | 460 | 180,000 | 2% |

2024 | 360 | 160,000 | 1% |

Audemars Piguet, celebrating its 150th anniversary, climbed to third by turnover with CHF 2.6 billion in sales, having multiplied revenues roughly fourfold since 2012 and moved to a distribution model where around 90% of sales pass through 72 mono‑brand boutiques and AP Houses. Patek Philippe, fourth in turnover but third in value share, remained steadfastly conservative on volume (~72,000 watches), compounding growth through mix and rising ASP, it now commands a retail share (7%) larger than the entire LVMH watch division (5.3%). Richard Mille, with a catalog of merely 29 references and 42 own boutiques, continued to push ever higher, with ASP near CHF 300,000 and an estimated 17% share of the CHF 125,000‑plus segment.

Audemars Piguet - Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2025 | 2,600 | 53,000 | 6% |

2024 | 2,380 | 51,000 | 5% |

Patek Philippe - Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2025 | 2,500 | 72,000 | 7% |

2024 | 2,300 | 72,000 | 7% |

Richard Mille - Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2025 | 1,750 | 5,950 | 4% |

2024 | 2,500 | 5,700 | 3% |

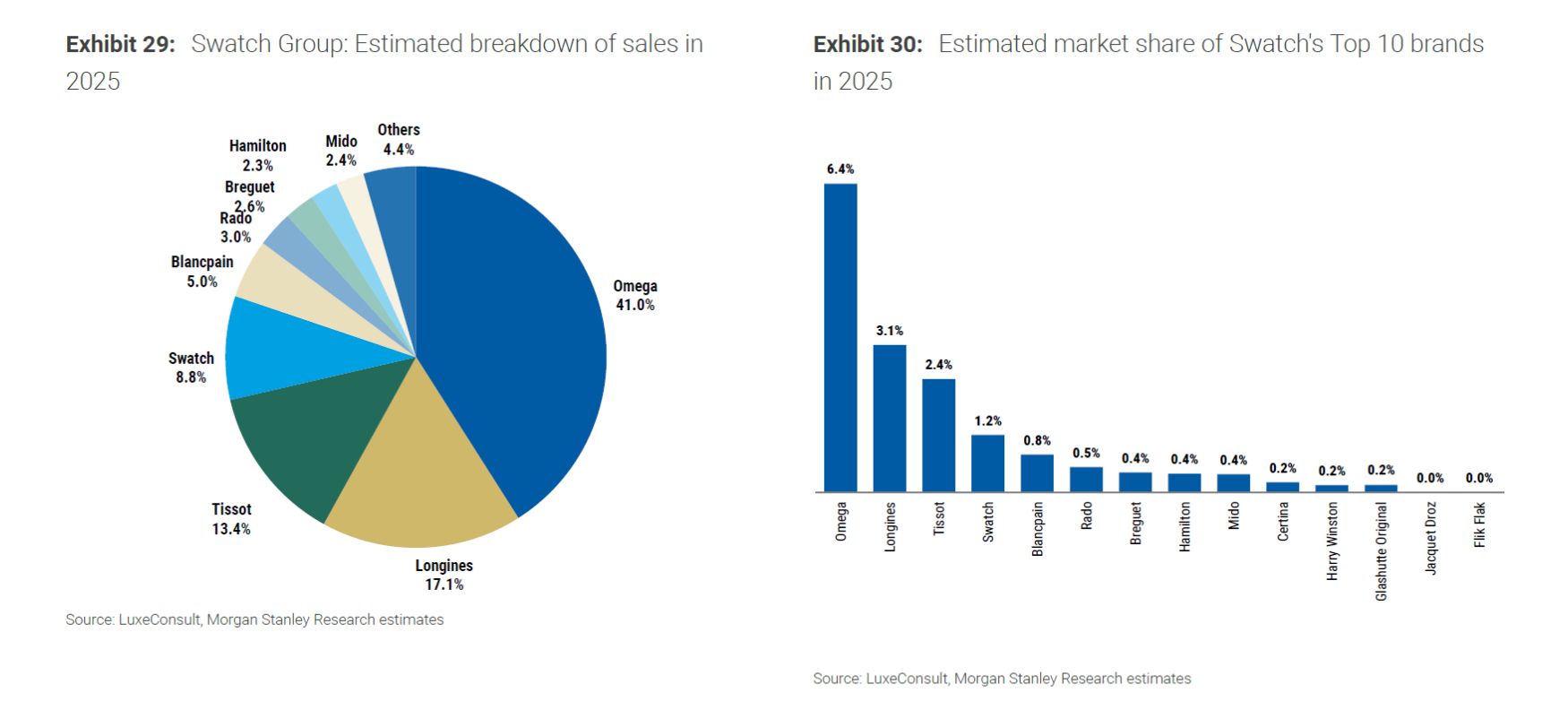

The picture is far less flattering for the big listed groups. Swatch Group remains the main “market share donor”, its overall share down to 16.1% in 2025, a drop of 220 bps in a single year and more than 1,000 bps since 2019. All of its top five brands: Omega, Longines, Tissot, Swatch, Blancpain, saw turnover decline in 2025, and some of the sharpest contractions in the Top 50 (Longines - 18%, Swatch - 15%, Hamilton, Blancpain, Breguet) are clustered inside its portfolio.

Omega, once the clear number two behind Rolex, slipped to fifth place, with sales stagnating around CHF 2.2 billion and a market share that has eroded from ~9% in 2017 to 6.4% in 2025, even as Rolex went from the low‑20s to nearly a third of the market. Group‑wide, Omega now generates roughly 80% of Swatch’s Watches & Jewelry operating profit, leaving the conglomerate heavily dependent on a single brand.

Omega - Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2025 | 2,210 | 460,000 | 6% |

2024 | 2,390 | 505,000 | 7% |

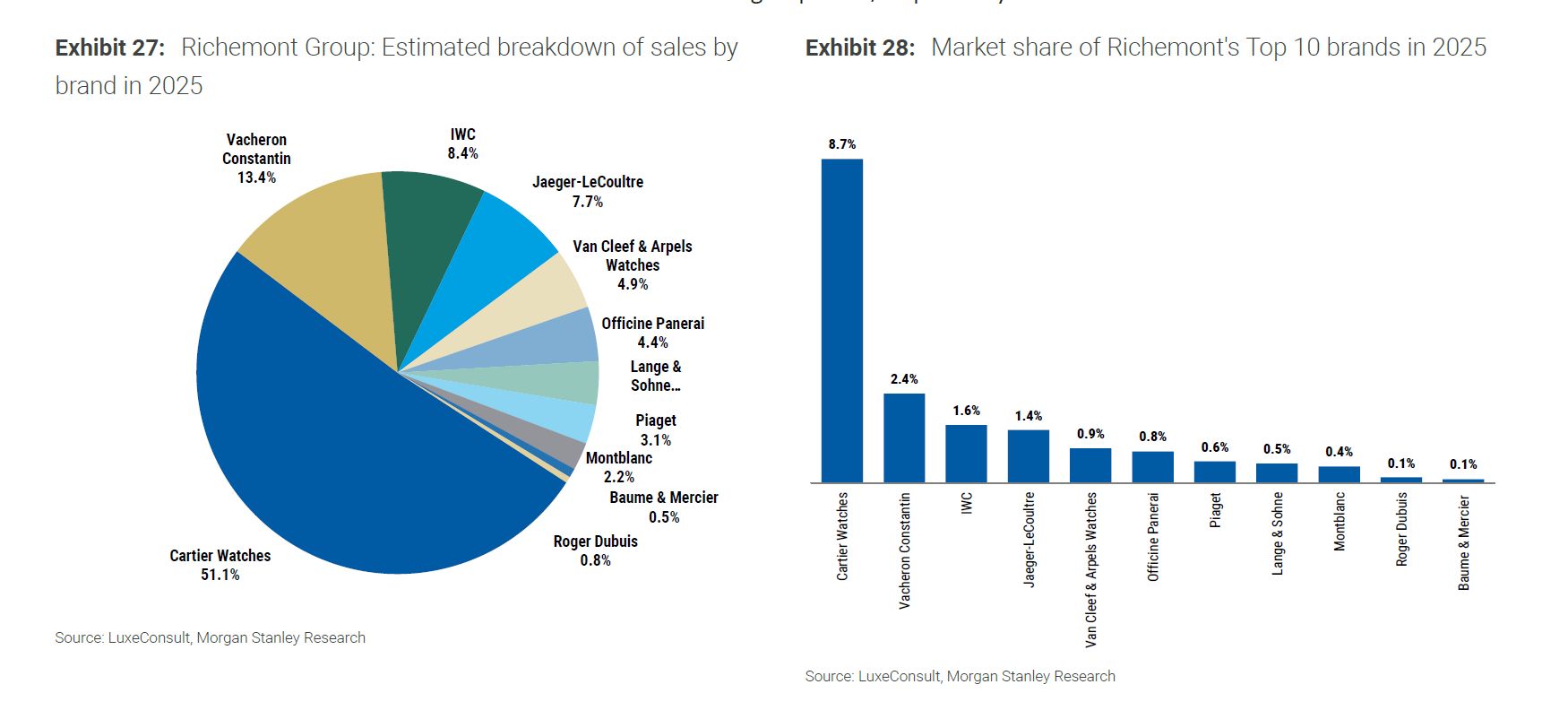

Richemont fared better but reveals a portfolio split. Cartier Watches, with CHF 3.5 billion in sales and an 8.7% market share, is the standout listed winner, having added roughly 300 bps of share since 2019 by combining accessible entry points (Tank Must at ~CHF 3,150) with high‑end horology and strong secondary‑market performance. Vacheron Constantin has also quietly outperformed, while the Specialist Watchmakers division as a whole saw market share slip to 7.6%, about 270 bps below 2019, as IWC, Jaeger‑LeCoultre, Piaget and Panerai struggled.

CARTIER Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2025 | 3,488 | 695,000 | 9% |

2024 | 3,183 | 680,000 | 8% |

Vacheron Constantin - Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2025 | 914 | 30,000 | 2% |

2024 | 942 | 31,000 | 3% |

LVMH’s watch position, now about 5.3% share (down 20 bps), is mixed: TAG Heuer, Hublot and Zenith declined, while Bulgari, Louis Vuitton and Dior grew, leveraging wider brand ecosystems to support watch sales.

Winners, Losers, And The Long Tail

Within the Top 50, 29 brands declined year‑on‑year in 2025 and 14 of those saw double‑digit drops, seven of them at Swatch Group alone. At the same time, the number of brands growing increased to 20 (from 12 in 2024), underlining a widening dispersion: success is less about “being Swiss” and more about positioning, distribution control, and pricing power.

At the entry and mid‑price levels, traditional names such as Longines and Tissot increasingly face competition from agile independents and micro‑brands with focused offerings and direct‑to‑consumer models. Christopher Ward, entering the Top 50 at rank 48 with ~CHF 51 million in sales and an ASP around CHF 1,300, is emblematic of this shift, delivering “Swiss Made” specifications in a pure DTC framework while scaling a community‑centric brand.

At the top end, the independents that matter - F.P. Journe, H. Moser & Cie., MB&F - continue to strengthen, with all three estimated to have grown in 2025 and now sitting between roughly CHF 50-125 million in sales on tiny production numbers. They remain small in macro terms but punch far above their weight in influence and desirability.

Smartwatches, Tariffs, And The Externalities

Smartwatches remain a separate universe in volume terms - about 85 million units in 2025 versus 14.6 million Swiss watches - but an increasingly overlapping one in pricing. Apple Watch Ultra 3, launched successfully in 2025, now competes squarely with entry‑level Swiss mechanicals such as the Tissot PRX Automatic in both price and perceived utility. After two years of revenue contraction, the smartwatch market returned to growth (Apple +15% estimated), but early signs of lengthening replacement cycles are appearing.

On the cost side, Swiss watchmakers faced a potent cocktail: US tariffs that swung between 10% and 39% before settling at 15%, Swiss franc appreciation of roughly 15% versus the US dollar, and a 65% year‑on‑year jump in gold prices - all of which fed through into the kind of price increases that now define the upper tiers of the market. That Rolex can raise average prices roughly 50% in six years and still grow share is less a testament to inflation than to the enduring strength of a handful of brands in a structurally constrained supply environment.

What The 2025 Report Really Says

Strip away the tables and the acronyms, and the Ninth Swiss Watchers report tells a story of a bifurcated industry. At one pole are four private maisons, vertically integrated, distribution‑tight, and increasingly in control of both primary and secondary markets, at the other is a fragmented ecosystem of listed conglomerates, historic names and ambitious independents trying to navigate shrinking volumes, demanding clients and unforgiving macroeconomics.

For collectors, that tension is visible every time a Land‑Dweller with a new escapement or a neo‑vintage Cartier design walks into the room and commands attention - while rows of competent but undifferentiated steel three‑handers linger in display cases. The Ninth Swiss Watchers report simply quantifies that intuition: in 2025, Swiss watchmaking became less about how many watches Switzerland exports, and more about which names are written on the dial.

No articles found