Ethos Limited Delivers Stellar Growth In FY25: Revenue Surges 25% Amid Strategic Expansion

We’re at the peak of fiscal fourth-quarter earnings season, and a significant number of companies spanning various sectors have reported their Q4 performance recently. Ethos Limited, India’s premier luxury watch retail chain, has announced its audited financial results for Q4 and FY25, showcasing robust growth, strategic expansion and strong operational performance.

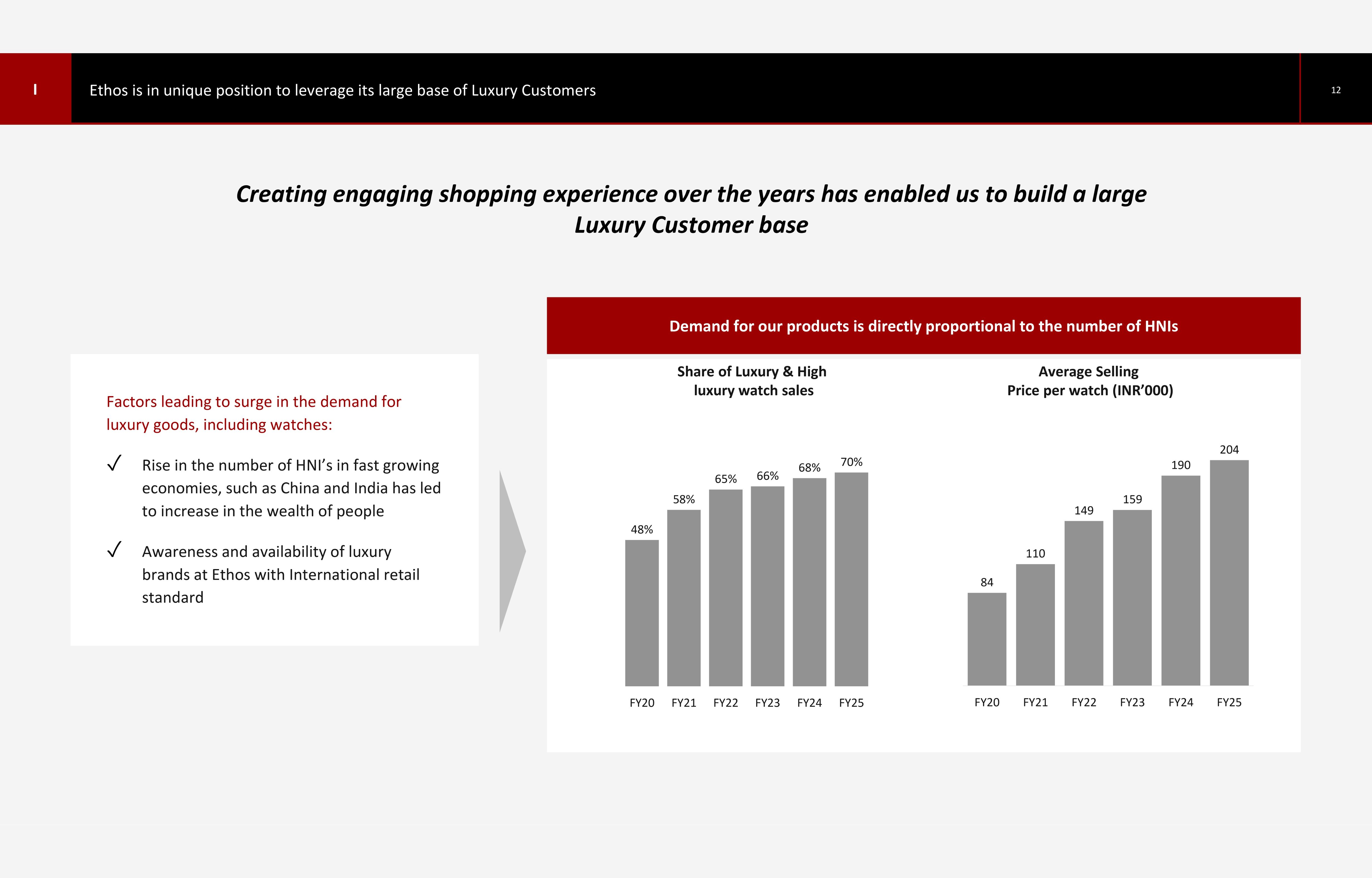

India’s quiet emergence as the Swiss watch industry’s next big growth market is a given of many factors among which the forecasted number of affluent Indians which is expected to reach 100 million people by 2027 is a contributing driver. Ethos plays a key role in enabling watch brands to capitalize on the growing demand for luxury timepieces in what is essentially one of the world’s most dynamic economies.

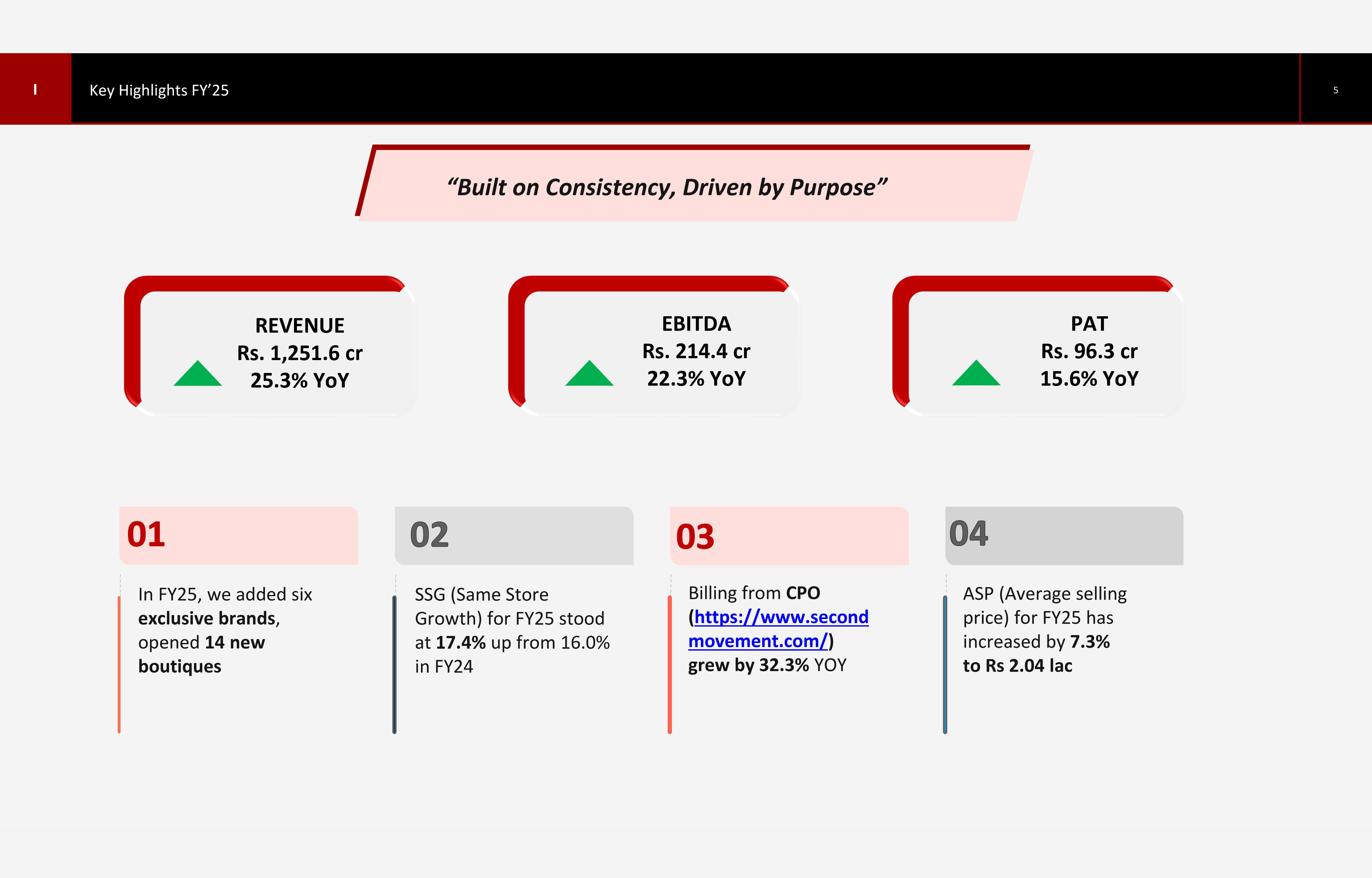

The company has delivered stellar growth in FY25, with revenue surging 25.3% YoY to ₹1,251.6 crore and EBITDA rising 22.3% to ₹214.4 crore. The company expanded its footprint to 73 boutiques across 26 cities, entered three new markets (Dehradun, Kochi and Mangaluru), and is set to open eight new stores in May 2025, including a flagship Messika jewelry boutique in Delhi.

This growth is driven by store expansions, higher average selling prices (ASP), and strong demand from high-net-worth individuals (HNIs).

Financial Performance: Breaking Down the Numbers

The numbers tell a compelling story of Ethos’s financial health. With double-digit growth across all key metrics, the company demonstrated both scale and resilience. But beyond the headline figures lie important nuances about margins, profitability, and the cost of expansion.

Revenue Growth - Sustained Momentum

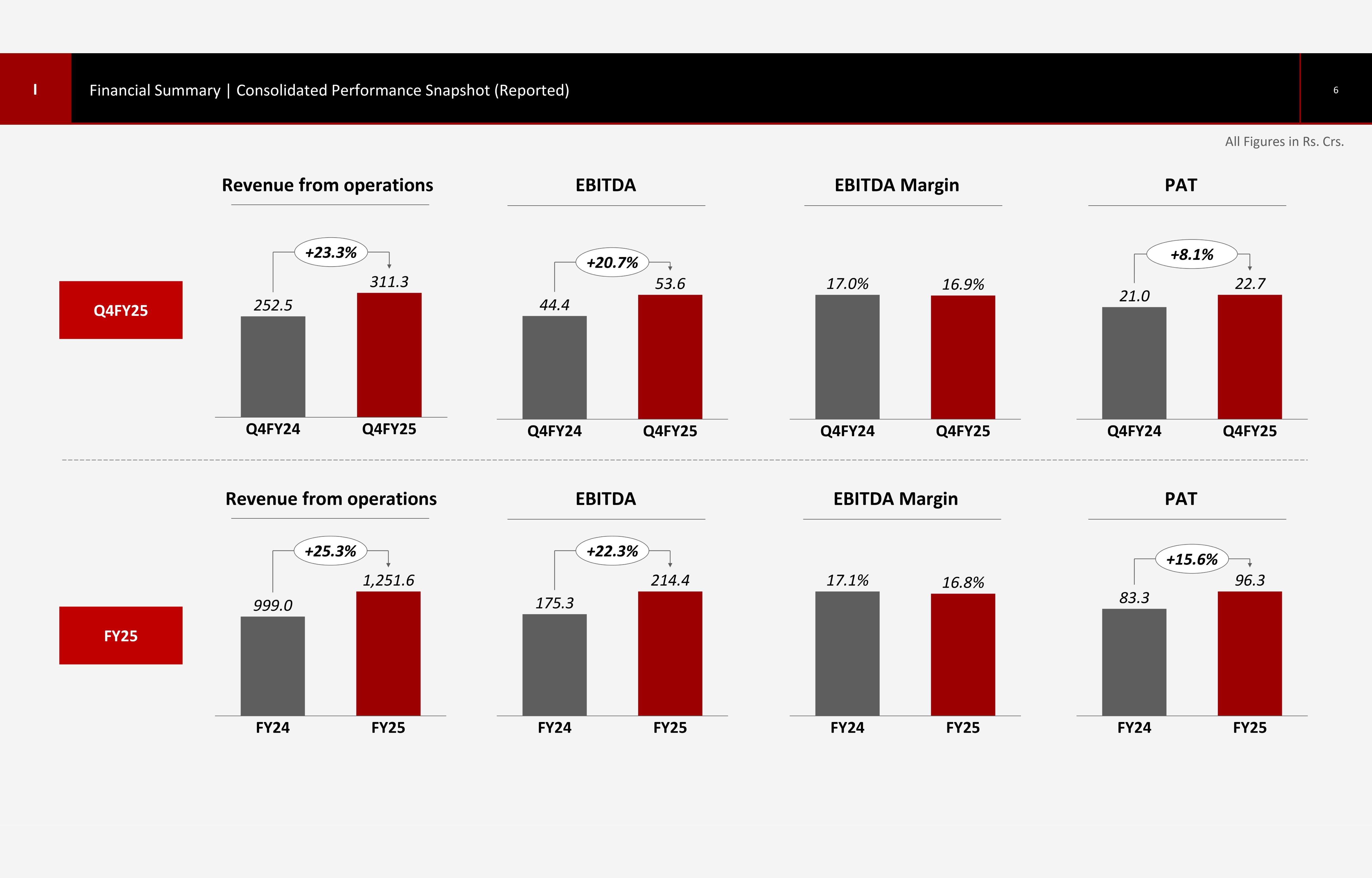

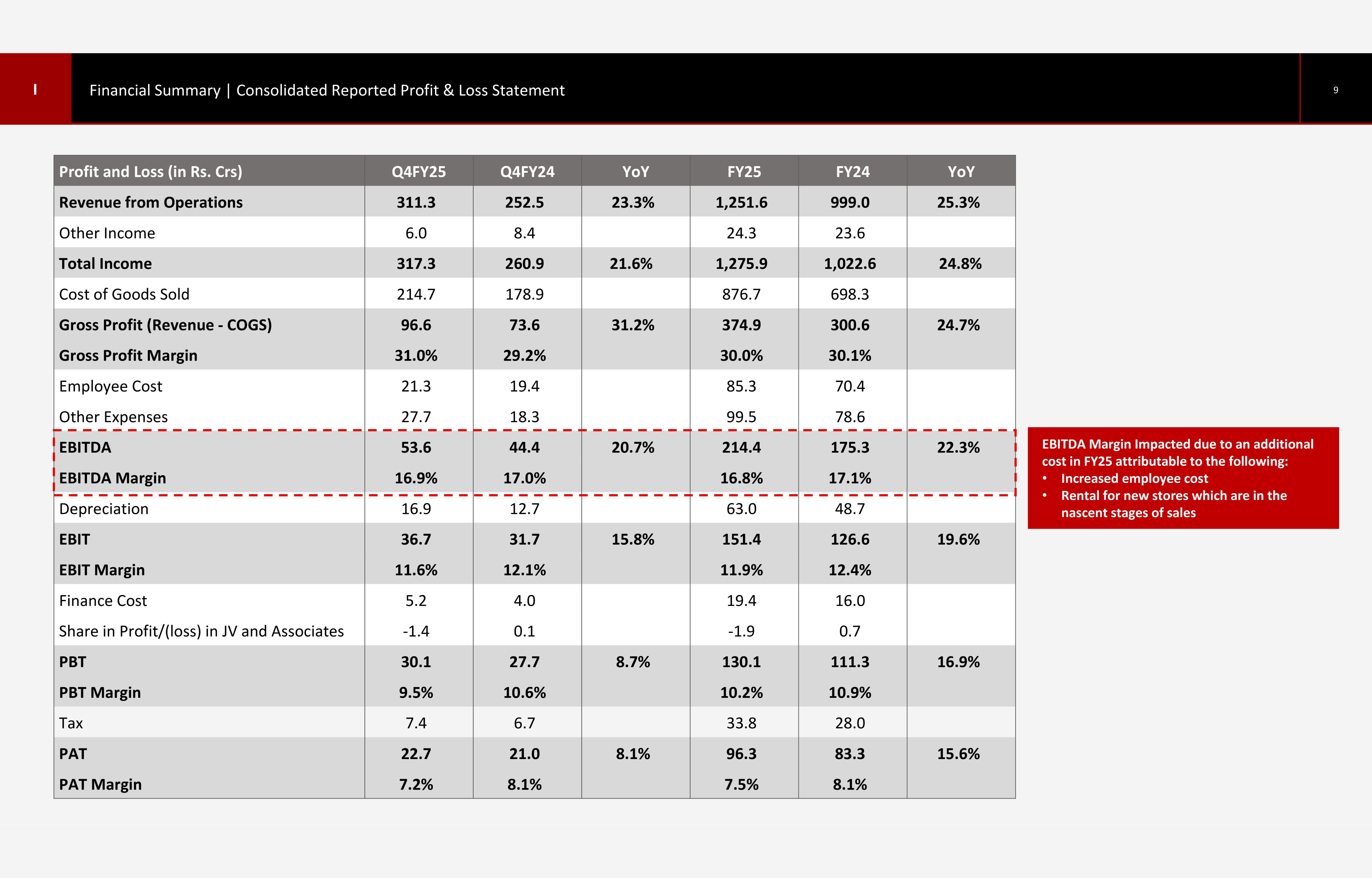

- Q4 FY25 Revenue: ₹311.3 crore (up 23.3% YoY from ₹252.5 crore in Q4 FY24).

- Full-Year FY25 Revenue: ₹1,251.6 crore (up 25.3% YoY from ₹999.0 crore in FY24).

- Same-Store Growth (SSG): 17.4% (vs. 16.0% in FY24), indicating strong organic demand.

What factors led to the growth?

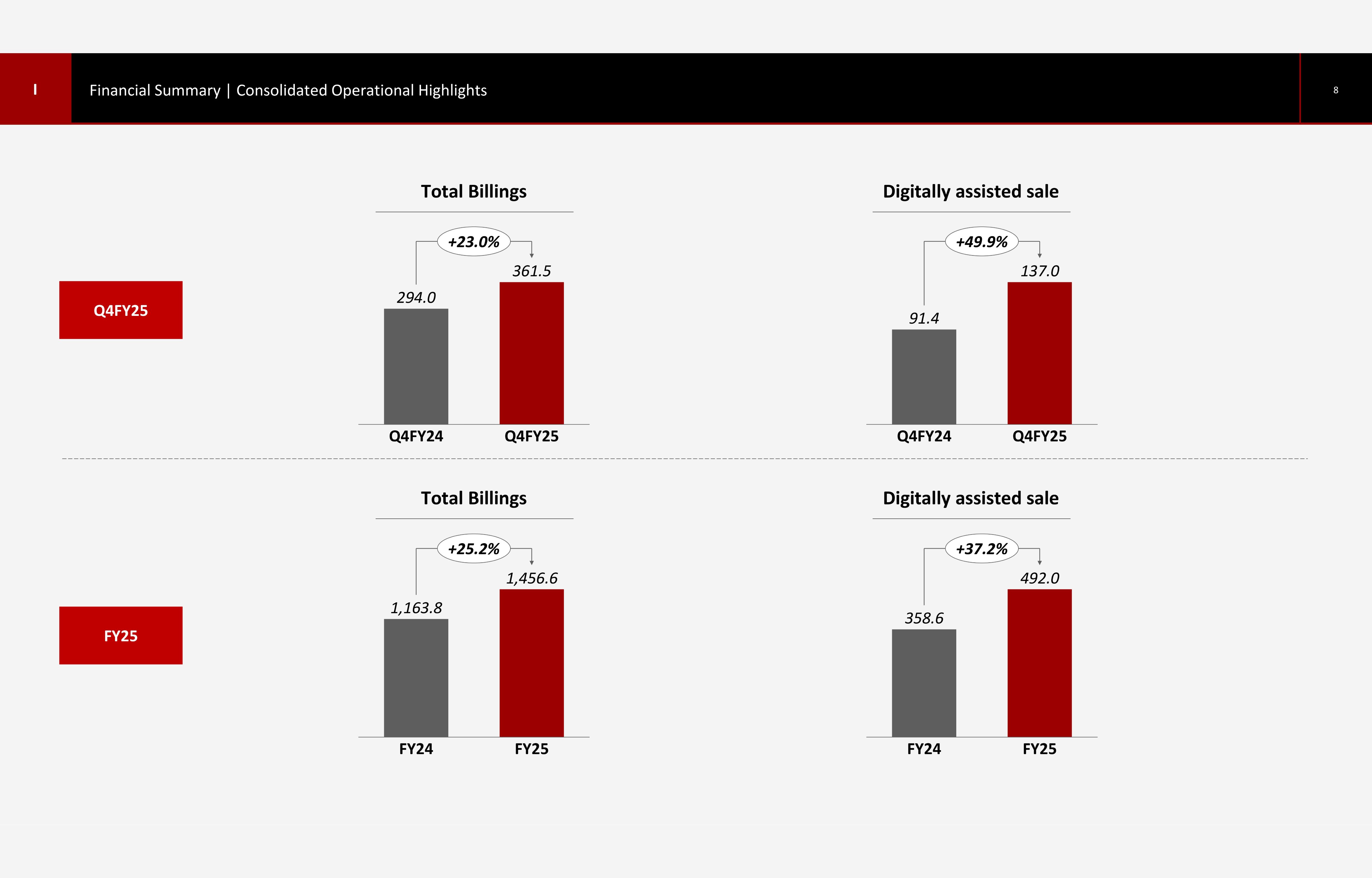

Among the principal growth drivers for revenue growth are the higher ASP (Average Selling Price): ₹2.04 lakh per watch (up 7.3% YoY) and the group’s expansion into new markets (Dehradun, Kochi, Mangaluru). Also, the rise of digitally assisted sales (up 49.9% YoY in Q4) has attributed to the favorable numbers.

Profitability - Margin Pressure from Expansion

- EBITDA for Q4 FY25: ₹53.6 crore (up 20.7% YoY).

- Full-Year EBITDA: ₹214.4 crore (up 22.3% YoY).

- EBITDA Margins: 16.8% for FY25 (vs. 17.1% in FY24).

Why Margins Contracted Slightly?

The slight moderation in EBIDTA margins has been attributed to the group’s new store investments with 14 boutiques added in FY25, calling for initial ramp-up costs. Also impacting the contraction are the higher employee and rental costs associated with this strategic expansion. In the management’s view, as expressed by Mr. Pranav Saboo - MD & CEO Ethos Limited, “This slight moderation aligns with our deliberate investments in talent and infrastructure, especially for newly launched stores that are still ramping up.”

PAT Growth - Steady but Impacted by Costs

- Profit After Tax (PAT): ₹96.3 crore (up 15.6% YoY).

- PAT Margins: 7.5% (vs. 8.1% in FY24).

While PAT grew, higher depreciation and finance costs (from leases) impacted bottom-line growth.

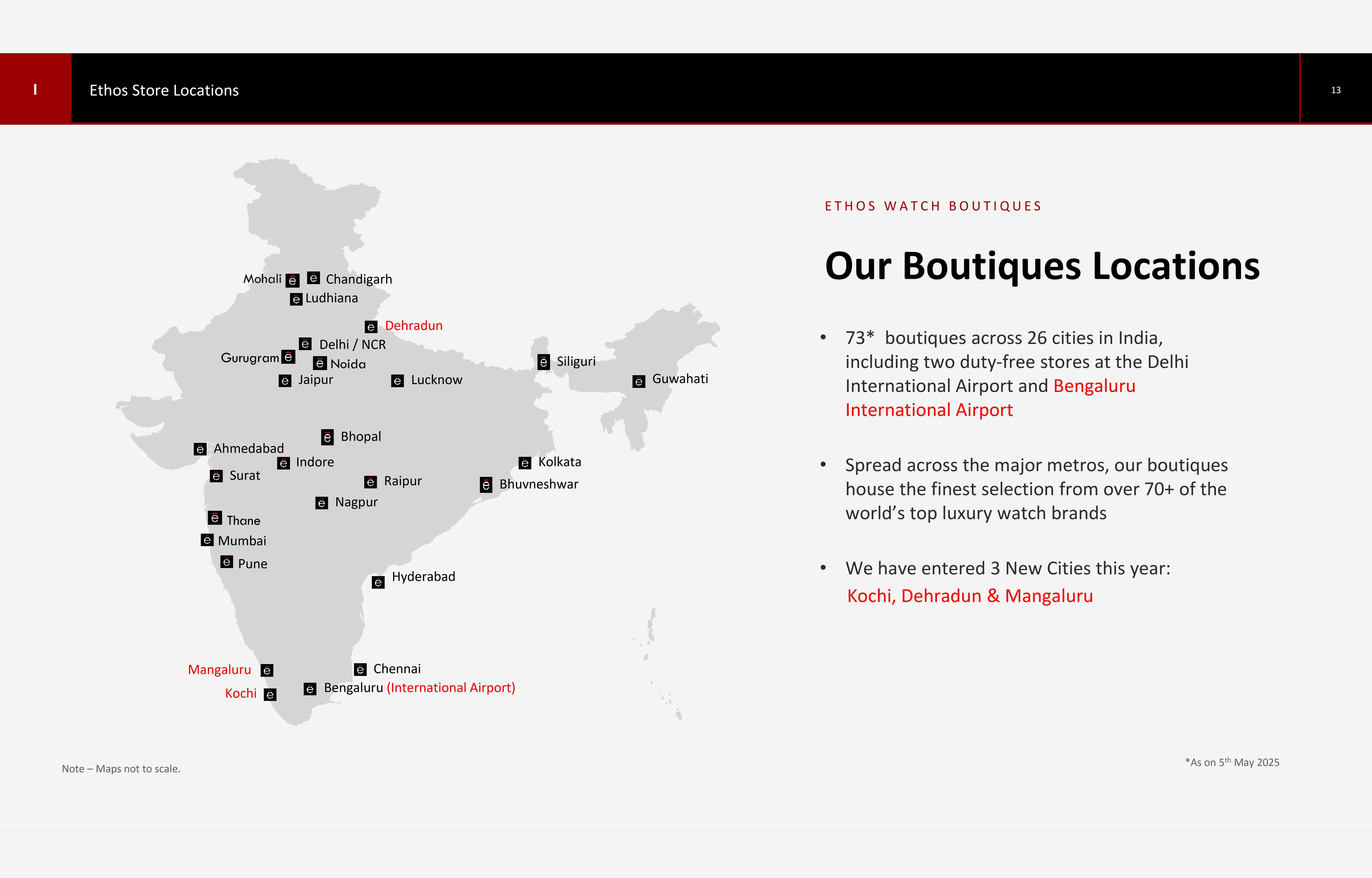

Store Expansion: Building India’s Largest Luxury Watch Retail Network

Physical retail remains at the heart of Ethos’s growth strategy. The company’s aggressive boutique expansion - adding 14 new stores in FY25 and entering three new markets, showcases its commitment to dominating India’s luxury landscape. Below, we explore their geographical playbook and what their upcoming store openings reveal about future ambitions.

FY25 Expansion Highlights

- Total Boutiques: 73 (up from 59 in FY24).

- New Markets Entered: Dehradun, Kochi and Mangaluru.

- Duty-Free Presence: Second boutique at Bengaluru International Airport.

Upcoming Launches (May 2025)

- 8 new boutiques, including: Flagship Messika Boutique (Delhi) - First exclusive store for the French luxury jewellery brand.

- Expansion in high-potential Tier 2 cities.

Why This Matters?

The partnership with Messika signals Ethos’s push into luxury jewellery, complementing watches. By scaling its presence in the Duty-Free space, the group capitalizes on opportunities posed by the rising international travel footprint.

Luxury Portfolio: Six New Marquee Brands Added in FY25

A luxury retailer is only as strong as its brand portfolio. Ethos made strategic moves in FY25 by adding six exclusive watch and jewelry brands to its list of offerings. This section breaks down each new partnership and what it means for Ethos’s positioning in the ultra-premium segment.

Ethos strengthened its luxury appeal by adding the following brands to its portfolio.

Brand | Origin | Specialization |

Christian Van Der Klaauw | Netherlands | Astronomical Complications |

Carl Suchy & Söhne | Austria | Austrian Heritage Timepieces |

Zero Halliburton | USA | Luxury Aluminium Luggage |

Hautlence | Switzerland | Avant-Garde Watchmaking |

ID Geneve | Switzerland | Sustainable Swiss Luxury |

Singer Reimagined | Switzerland | Automotive-Inspired Watches |

What’s the strategic Impact of this expanded curation?

By adding six new marquee brands to its portfolio, Ethos has diversified its revenue streams beyond watches while also attracting ultra-HNI clientele seeking exclusivity.

Management’s Vision: 10x Revenue Growth in a Decade

Ethos Limited’s CEO Pranav Saboo’s bold vision of 10x revenue growth isn’t just aspirational - it’s backed by a clear strategic playbook. The key growth levers for the management range from talent investment to operational excellence.

Key Growth Levers for FY26 and Beyond.

- Aggressive Retail Expansion: Targeting 100+ stores in the medium term.

- Digital and Omnichannel Push: Digitally assisted sales up 49.9% YoY.

- Premiumization: ASP growth (₹2.04 lakh per watch) reflects pricing power.

- CPO (Certified Pre-Owned) Segment: 32.3% YoY growth - a high-margin opportunity.

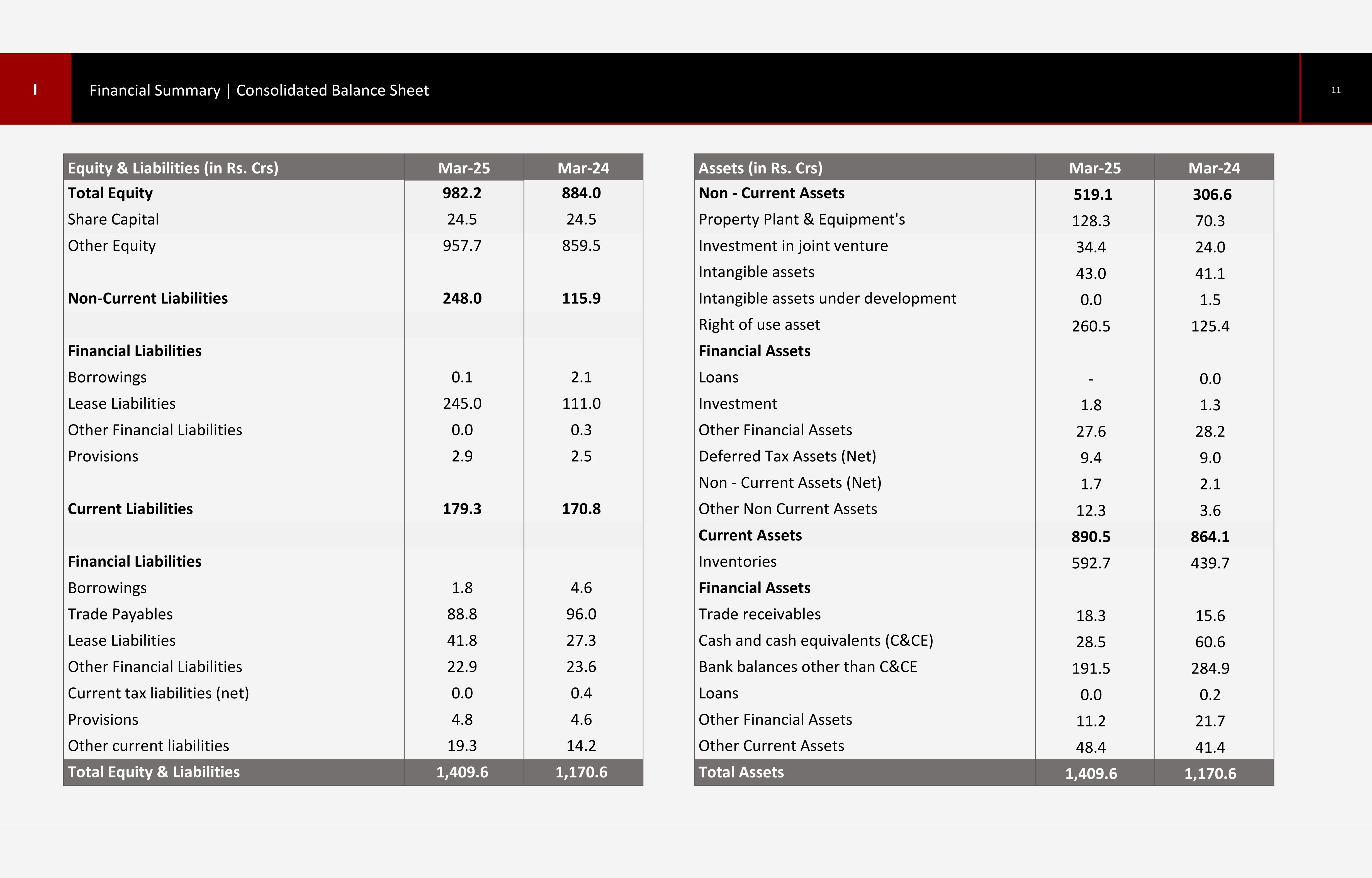

Financial Health: Strong Balance Sheet with Controlled Leverage

Ethos’s financial foundations remain robust despite expansion costs. In their published balance sheet, one can analyze their liquidity position, inventory management, and capital structure to assess long-term sustainability. The key highlights are stated as follows.

- Cash and Equivalents: ₹28.5 crore (down from ₹60.6 crore due to expansion spend).

- Inventory: ₹592.7 crore (up 34.8% YoY) - stocking up for new stores.

- Debt Position: Minimal borrowings, with strong equity (₹982.2 crore).

What’s Next? Key Catalysts to Watch

While the FY25 story is complete, Ethos’s growth journey is just getting interesting. From upcoming store launches to margin recovery timelines, the milestones that could drive the next phase of value creation for shareholders remain to be the future triggers of growth for the group and its investors.

Keep an open eye for the following.

- Q1 FY26 Results (Aug 2025): Early signs of margin normalization.

- New Store Openings: 8 boutiques in May 2025.

- CPO Segment Growth: Could be a hidden gem for margins.

Bottom Line: Ethos is executing a winning playbook - luxury retail expansion, premium brand curation, and digital integration. The 10x revenue vision fostered by Pranav Saboo - MD & CEO, looks ambitious but achievable given India’s booming luxury appetite.

Quick Stats at a Glance (FY25)

Metric | FY25 Performance | YoY Growth |

Revenue | ₹1,251.6 cr | 25.30% |

EBITDA | ₹214.4 cr | 22.30% |

PAT | ₹96.3 cr | 15.60% |

Store Count | 73 | +14 stores |

ASP per Watch | ₹2.04 lakh | 7.30% |

Why Ethos Stands Out?

For investors and luxury enthusiasts alike, Ethos represents a front-row seat to India’s luxury retail revolution. As disposable incomes rise and brand consciousness grows, Ethos is delivering consistent double-digit growth, despite operating in a market where luxury retail is still somewhat nascent. Moreover, the group has masterfully positioned itself at the intersection of aspiration and accessibility in India’s booming luxury market.

The question isn’t if they’ll dominate, but how big they’ll become.