Richemont FY26 Results Decoded: €22 Billion, A 3.4% Watch Margin, And The Quiet Sale Of A Maison

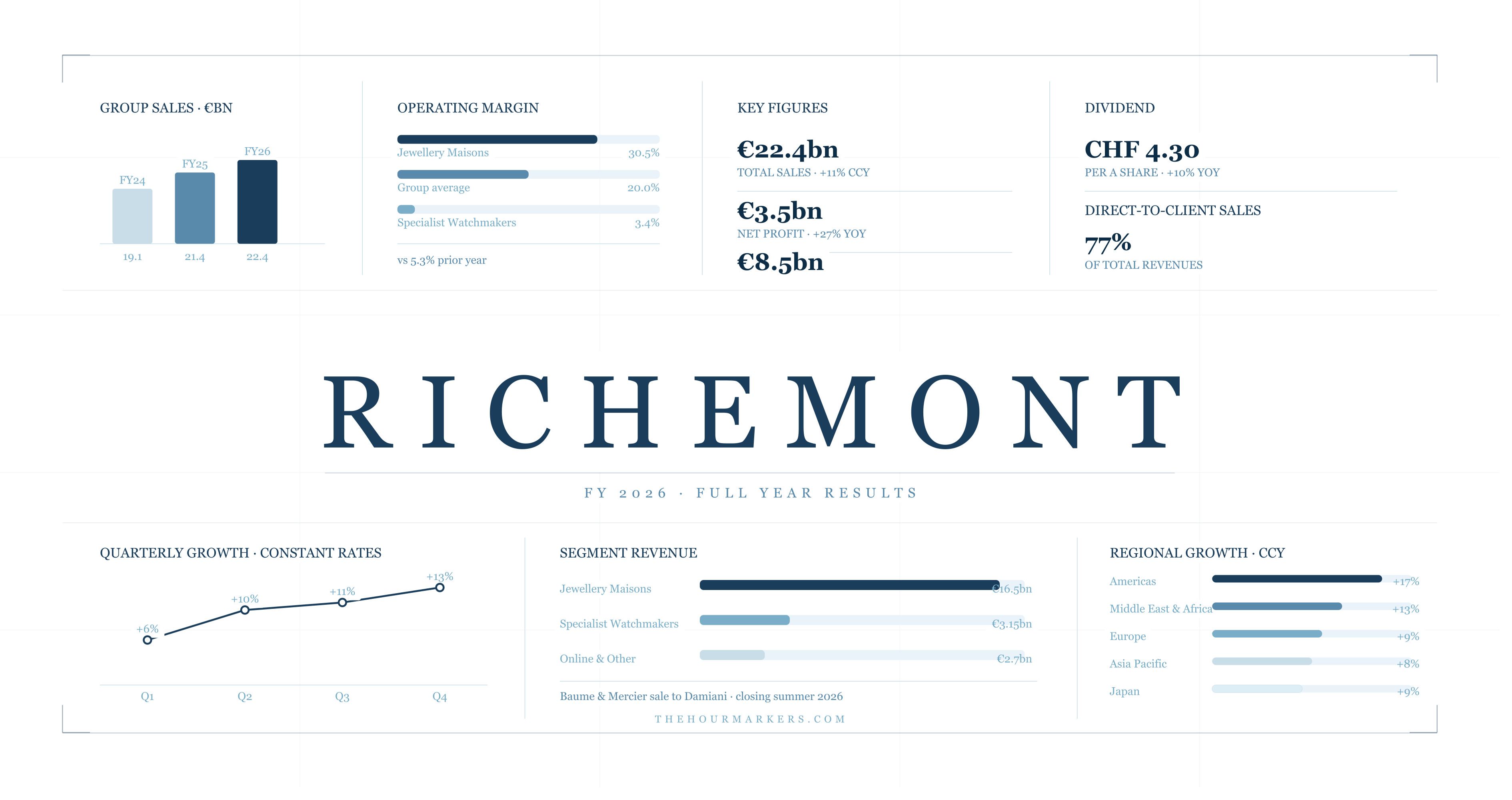

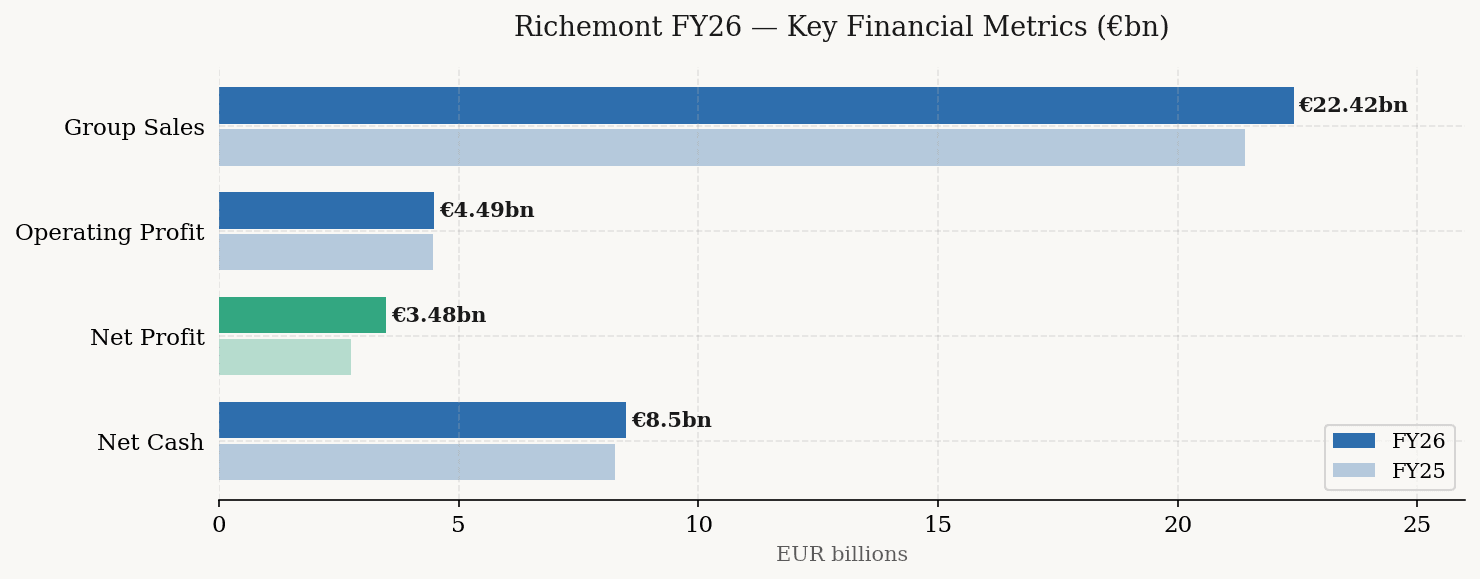

Richemont published its full-year results for FY26 on May 22, 2026. The headline is excellent: €22.4 billion in sales, up 11% at constant exchange rates. €3.5 billion in profit, up 27%. Net cash of €8.5 billion. A proposed ordinary dividend of CHF 3.30 per A share plus a special dividend of CHF 1.00, up 10% year-on-year. Chairman Johann Rupert's closing remarks were measured and confident. The watch community should read the next layer down, because the picture there is considerably more complicated.

The Two-Speed Company

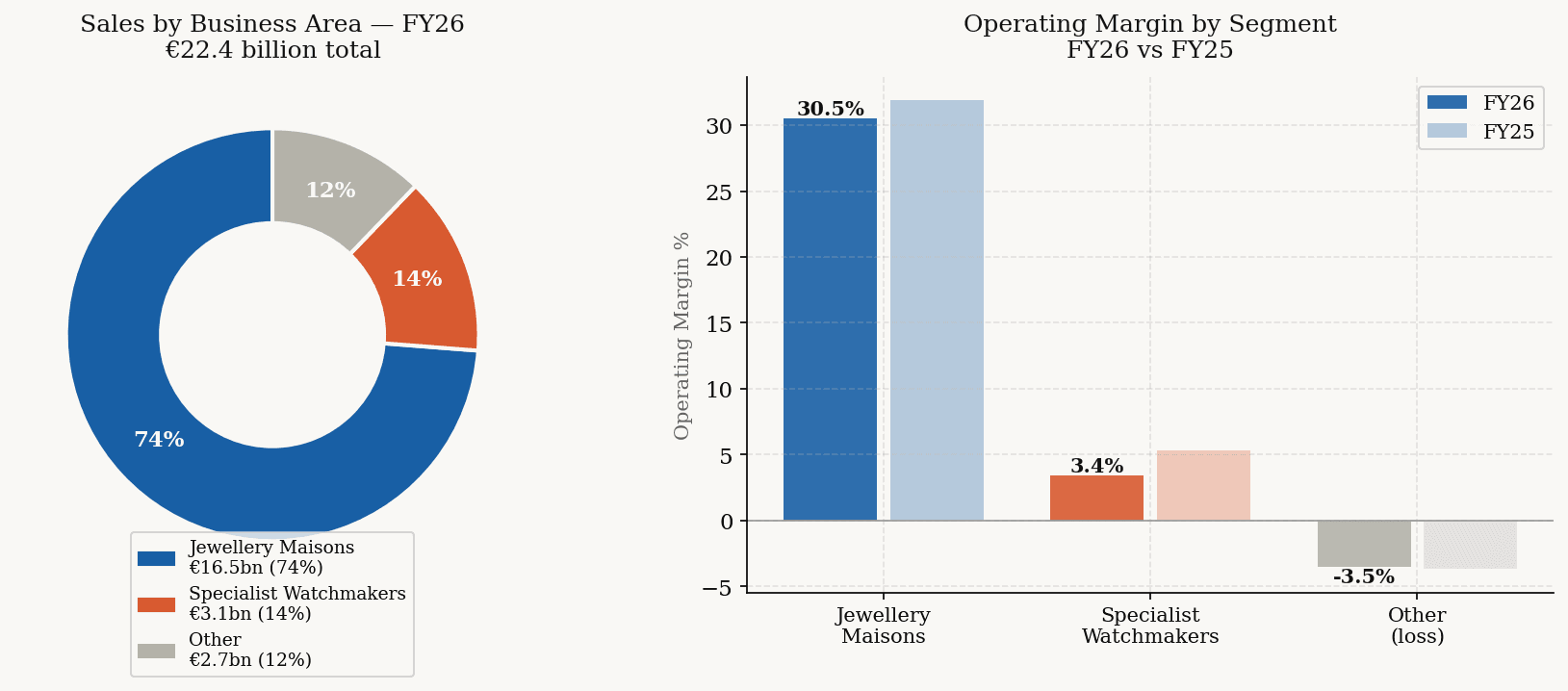

Richemont operates three business areas. Jewellery Maisons, which encompasses Cartier, Van Cleef & Arpels, Buccellati, and Vhernier, generated €16.5 billion in sales, up 8% at actual rates and up 14% at constant rates. Their operating margin was 30.5%, delivering €5 billion in operating profit. Specialist Watchmakers, which comprises A. Lange & Söhne, IWC Schaffhausen, Jaeger-LeCoultre, Panerai, Piaget, Roger Dubuis, Vacheron Constantin, and Baume & Mercier, generated €3.15 billion in sales, down 4% at actual rates, up just 1% at constant rates. Their operating margin was 3.4%, delivering €107 million in operating profit.

The jewellery business is nine times larger by revenue and nine times more profitable by margin than the watch business. The watches that watch enthusiasts actually follow, the manufactures, the complications, the collector-grade pieces, contribute less to Richemont's bottom line than rounding errors in the Cartier jewellery division. This is not a new structural reality. But it has never been stated quite as starkly as it is in these charts.

The Watch Margin Collapse

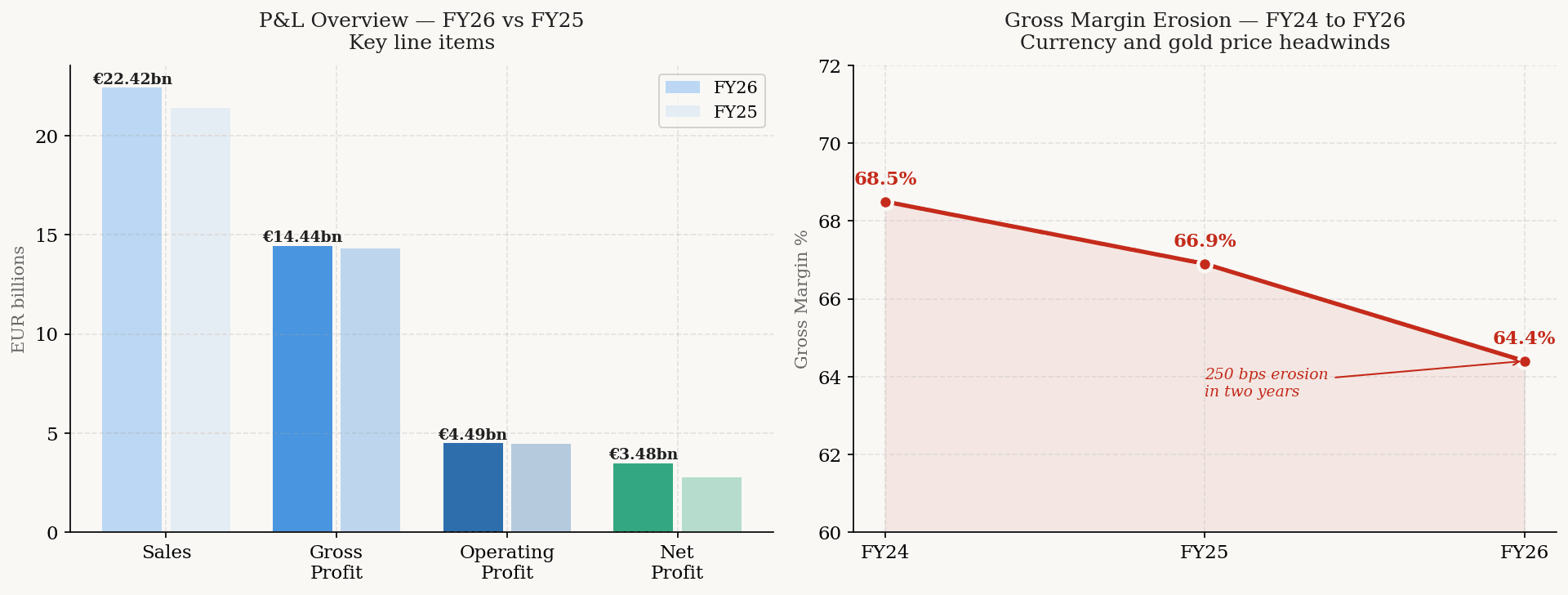

The Specialist Watchmakers' 3.4% operating margin is the single most important number in this document for anyone who cares about the watch industry's financial health. To put it in context: Richemont's Jewellery Maisons operate at 30.5%. The broader Group operates at 20%. Apple, for reference, operates at roughly 30%. A 3.4% margin means that on every €100 of watches sold by Jaeger-LeCoultre, Panerai, IWC, or Vacheron Constantin, the business keeps €3.40 after costs. A year ago that margin was 5.3%. A year before that it was higher still. The trajectory is a line going in one direction.

Three forces are doing the damage simultaneously. First, currency. The Swiss franc strengthened materially against the euro, dollar, and yen throughout the year, meaning every watch priced in local currency generates fewer francs back in Switzerland than it did twelve months ago. Richemont estimates the total unfavourable currency impact on gross margin across the group at hundreds of millions. The watch division, where production costs are almost entirely denominated in Swiss francs, is disproportionately exposed.

Second, gold. The price of gold hit record levels in 2025 and has not retreated meaningfully. For a Jewellery Maison, gold is a cost that can be recouped through price increases. For a watch case in 18-karat gold, the same dynamics apply but with significantly less pricing flexibility in a market where steel watches dominate volumes. Third, fixed costs. When a manufacture produces fewer watches, the fixed costs of running the manufacture, the master watchmakers, the machinery, the lease on the building, do not reduce proportionally. They stay largely fixed while the revenue line falls. The resulting deleveraging effect crushed the operating profit to €107 million on a revenue base of €3.15 billion.

The Baume & Mercier Signal

Buried in the financial notes but significant in what it implies: on January 22, 2026, Richemont announced it had signed an agreement to sell Baume & Mercier to the Damiani Group, the Italian family-owned luxury jeweller. Closing is expected in summer 2026. The write-down associated with the sale contributed €59 million of the €164 million in non-recurring costs that sit inside the operating profit line. The Baume & Mercier assets and liabilities have been reclassified to disposal groups on the balance sheet.

This is the first time in recent memory that Richemont has divested a watch Maison. The rationale offered by management is coherent: Baume & Mercier's predominantly multi-brand wholesale distribution model, its accessible luxury positioning, and its Italian retail strength make it a better fit for Damiani than for Richemont's increasingly direct-to-client, boutique-focused operating model. There is no reason to doubt this explanation. But it is also true that Baume & Mercier occupies the most price-sensitive segment of the Specialist Watchmakers portfolio, where margin pressure from currency and material costs lands hardest. A watch retailing at CHF 3,000 has far less pricing power than one retailing at CHF 30,000. In an environment where every franc of margin counts, the calculus of which watches to keep and which to let go is becoming more explicit.

Where the Growth Actually Came From

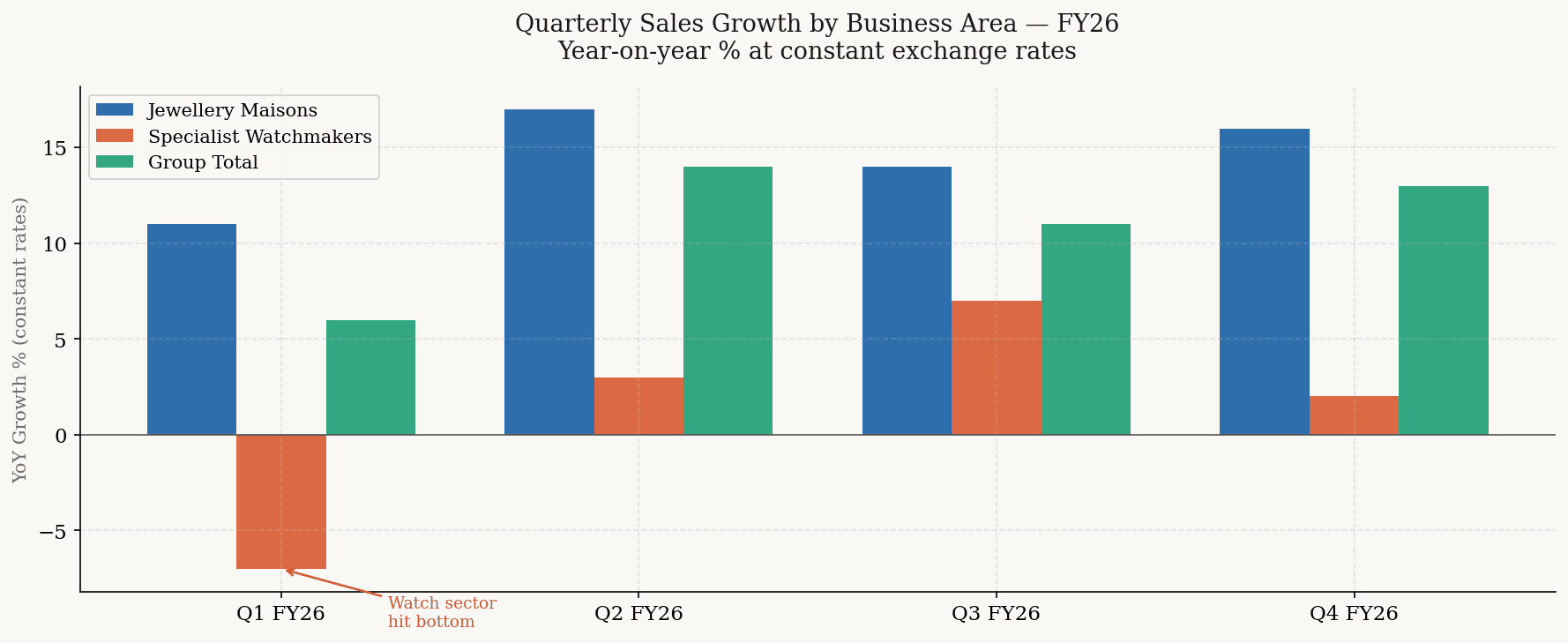

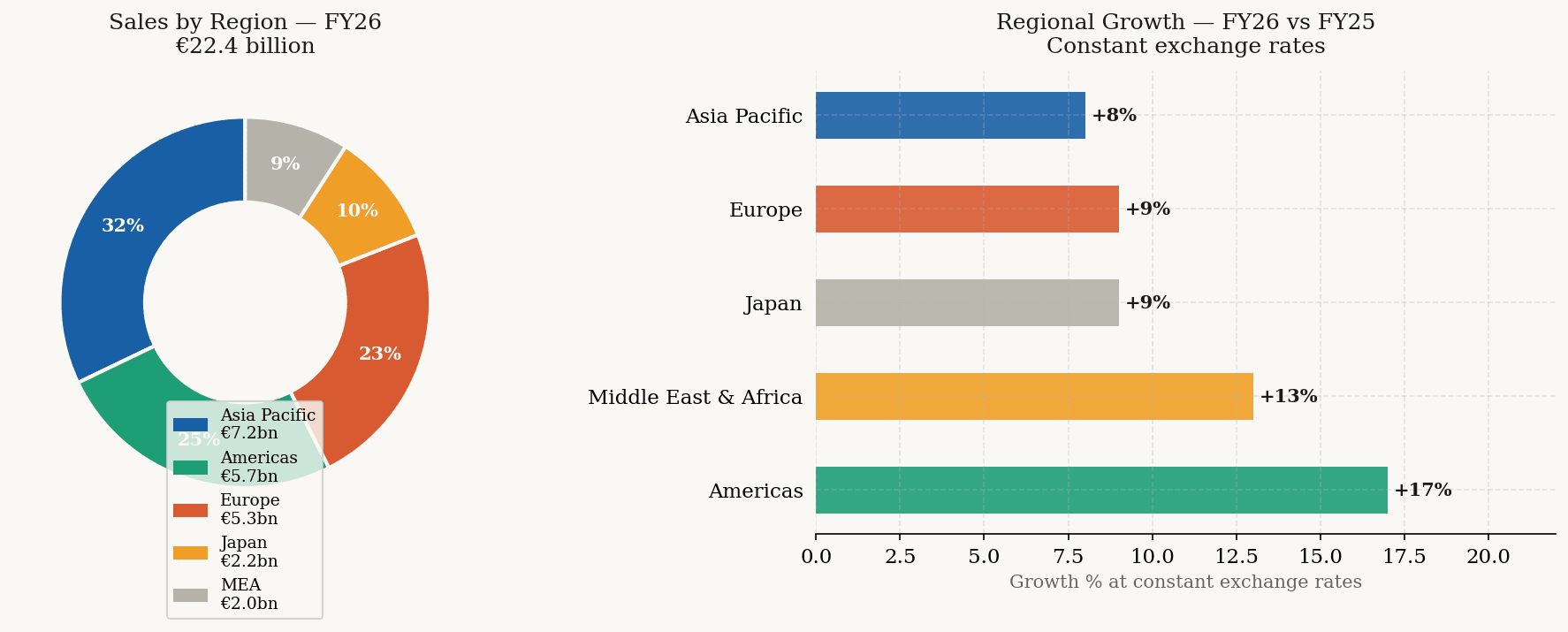

The Americas posted 17% growth at constant exchange rates, the strongest regional performance in the group. Double-digit growth every quarter of the year, including 18% in Q4. Both Jewellery Maisons and Specialist Watchmakers grew by double digits in the region. The US market, despite the 39% tariff that hit imports between August and November 2025, remained the most resilient luxury consumption engine in the world. This partly reflects front-loading before the tariff increase and partly reflects the underlying strength of the US consumer in the luxury segment.

Asia Pacific recovered to 8% growth at constant rates, led by South Korea at almost €1.4 billion in sales. China, Hong Kong, and Macau combined grew by 3% at constant rates, an improvement over the prior year's decline but still far below the pre-2023 baseline. The fourth quarter was the strongest in the region at 14% growth, suggesting momentum building into FY27. Japan grew 9% at constant rates for the full year, accelerating to 28% in Q4, its strongest quarterly performance in years, driven entirely by local demand rather than tourist spend. The Middle East and Africa grew 13% at constant rates for the year but contracted 3% in Q4 as the conflict in the region disrupted local demand and tourist flows in March. Europe grew 9%, supported by local demand and positive tourist spend in the first half, moderating to 5% in Q4 against elevated prior-year comparatives.

The Channel Shift

Retail sales, from the group's 1,393 directly operated boutiques, grew 12% at constant rates and now represent 71% of total group sales. Combined with online retail at 6%, direct-to-client sales account for 77% of Richemont's total revenues. For the watch industry, this is structurally significant. When a Richemont watch sells through a directly operated boutique, Richemont captures the full retail margin. When it sells through a multi-brand retailer like Ethos or Art of Time, Richemont captures only the wholesale margin and the retailer keeps the difference. The ongoing shift toward direct-to-client channels means Richemont is capturing more of the value chain on each watch sold. It also means that independent multi-brand retailers face a structural pressure that does not appear in their own sales numbers but is visible in the supplier's.

The Q4 Acceleration and What It Means for FY27

Q4 FY26, the quarter ended March 31, grew 13% at constant rates across the group. The Jewellery Maisons grew 16%. Specialist Watchmakers grew 2%. Both figures represent sequential improvement from the prior quarters. The Specialist Watchmakers recovery in Q4 was led by visible improvement at A. Lange & Söhne, Jaeger-LeCoultre, and Vacheron Constantin in the second half of the year. Panerai's depth-of-time exhibition programme, which toured Florence, New York, and Shanghai, and the JLC Reverso Tribute models contributed to this improvement. Whether the recovery is sustainable depends primarily on whether China, Hong Kong, and Macau continue their gradual return to growth, and whether the Swiss franc stabilises against major trading currencies.

Management's language in the results is cautious: "uncertainty is likely to persist, not least in relation to developments in the Middle East." The proposed special dividend of CHF 1.00 per share, on top of a 10% increase in the ordinary dividend, signals confidence in the cash position without overcommitting to an acceleration in the underlying business.

The Numbers That Matter for Watch Collectors

€3.15 billion in Specialist Watchmakers revenue divided by eight brands is an average of approximately €394 million per brand per year. In practice the distribution is highly uneven. Cartier's watch division alone likely exceeds the entire Specialist Watchmakers combined. Jaeger-LeCoultre and Vacheron Constantin are probably the largest among the eight. Roger Dubuis and A. Lange & Söhne are almost certainly the smallest. A 3.4% operating margin on €394 million average brand revenue is approximately €13.4 million per brand in operating profit. For a manufacture that employs hundreds of master watchmakers, maintains a network of boutiques, produces in-house movements, and runs global marketing programmes, €13.4 million in operating profit is thin. Very thin.

The conclusion is not that these brands are in trouble. They are not. Richemont's net cash position of €8.5 billion gives the group the financial depth to sustain the watch division through a margin-compressed period without existential concern.

Key Numbers at a Glance

Group sales: €22.42 billion. Up 5% actual, 11% constant.

Gross profit: €14.44 billion. Gross margin 64.4%, down from 66.9%.

Operating profit: €4.49 billion. Operating margin 20.0%, down from 20.9%.

Net profit: €3.48 billion. Up 27%, partly reflecting non-recurrence of the €1 billion YNAP write-down.

Jewellery Maisons: €16.54 billion in sales. 30.5% operating margin. €5.04 billion operating profit.

Specialist Watchmakers: €3.15 billion in sales. 3.4% operating margin. €107 million operating profit.

Net cash: €8.50 billion. Operating cash flow: €4.88 billion.

Dividend: CHF 3.30 ordinary plus CHF 1.00 special per A share. Payable September 2026.

Baume & Mercier sale to Damiani Group: closing expected summer 2026.