Morgan Stanley And LuxeConsult’s Top 50 Swiss Watch Brands For 2024

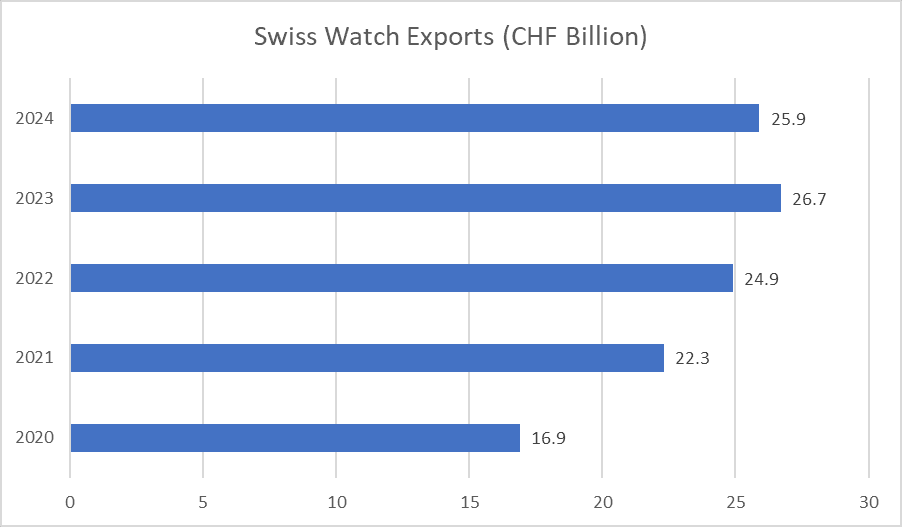

Maturation, plateauing and deceleration. Although these three terms commonly used in business-matters don’t necessarily indicate an industry in trouble, they sure raise a few alarms. The Swiss watch industry has been an enterprise perpetually tackling geopolitical uncertainties, demand fluctuations and shifting preferences in consumer behavior. Owing to such factors, we have an industry that, although fundamentally healthy in terms of long-term revenue prospects, depicts a picture that’s diverse in terms of individual brand performance and profit sustainability. As evident in the latest Morgan Stanley and LuxeConsult report on the Top 50 Swiss Watch Brands for 2024, the overall market reports a potential slowdown in terms of sales and this is concurrent with the latest numbers from the Swiss Federation of the Watch Industry (FHS). As per FHS, 2022 and 2023 were record years for the Swiss watch industry, which touched CHF 24.9 and 26.7 billion respectively in terms of overall exports. However, the year 2024 witnessed a downfall in exports by about 3% as the industry achieved a total of CHF 25.9 billion in export revenue. This slow-down phase of the industry first indicated in Morgan Stanley’s 2023 market report and now the latest annual report for 2024, which is the eighth instalment of its kind, confirms that the Swiss watch industry, following two consecutive years of robust growth, hasn’t been at its best in terms of sales revenues. Any exceptions, well yes - Rolex!

Performance Highlights: Swiss Watch Market in 2024

What has been evident for the concluding quarter of 2023 and the entire 2024 is that for the first time in recent years, the Swiss watch industry is facing a little bit of a challenge. For the last few years, referring to Covid and post-Covid times, the industry has had a tsunami of interest in watches. With speculators jumping in and the overall aspect of “investment” in regards to watches as an asset gaining traction, brands recorded impressive sales and as a result, watch prices in the primary as well as secondary markets rocketed upwards. But now we’ve come back to an era of sanity and rationalism and in this phase, we’ve a clear divide between the brands that are powerful and that’ll probably continue gaining market share and those that have kind of fallen off the radar by a bit. 2024 presented a challenging environment for the Swiss watch industry, with only 11 of the top 50 brands experiencing sales growth. The report by Morgan Stanley and LuxeConsult highlights key trends and performance indicators, revealing a market increasingly polarized and driven by a select few brands. Listed below are the brands which experienced sales growth in 2024 as compared to 2023.

Rank | Group | Brand |

1 | Rolex | Rolex |

2 | Richemont | Cartier Watches |

4 | Audemars Piguet | Audemars Piguet |

5 | Patek Philippe | Patek Philippe |

6 | Richard Mille | Richard Mille |

11 | LVMH | TAG Heuer |

17 | LVMH | Bulgari |

24 | Richemont | Van Cleef & Arpels Watches |

36 | Citizen | Frederique Constant |

37 | F.P Journe | F.P Journe |

38 | H. Moser & Cie | H. Moser & Cie |

50 | MB&F | MB&F |

Market Polarization and Dominance of the “Big Four”

The “Big Four” - Rolex, Patek Philippe, Audemars Piguet and Richard Mille - continue to consolidate their market dominance. Their combined market share reached an impressive 47%, representing a substantial 300 basis point increase year-over-year and a remarkable 1,020 basis point surge compared to pre-pandemic levels (36.8%). This concentration of power underscores a significant polarization within the industry.

Top Brands and Market Share Dynamics

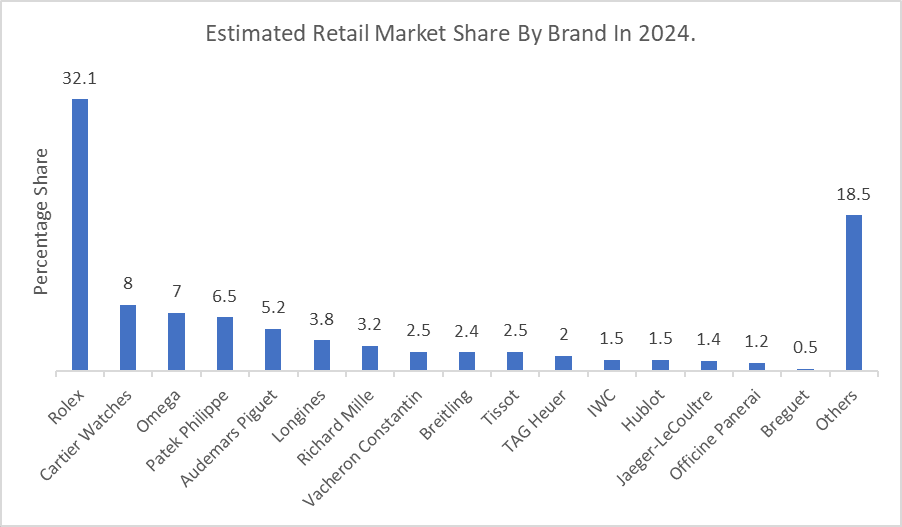

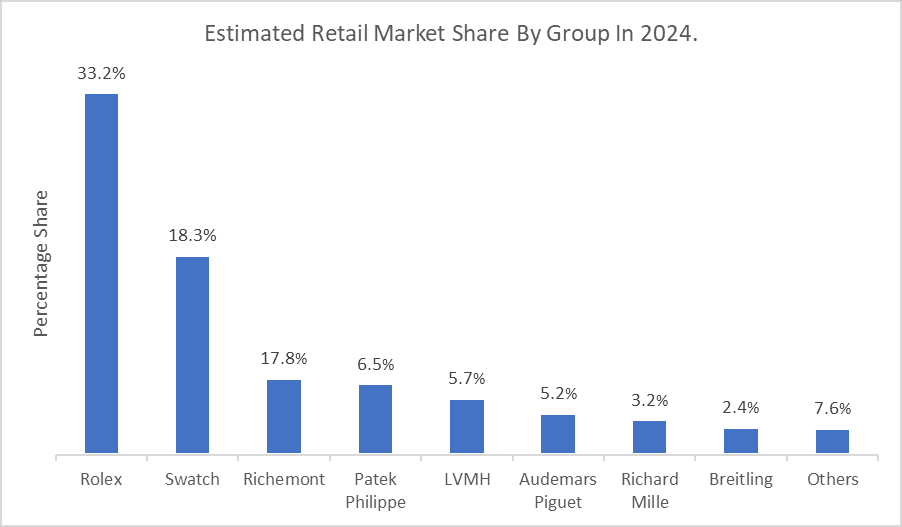

Out of approximately 400 Swiss watch brands, the top four (Rolex, Cartier, Omega and Patek Philippe) account for over 50% of total sales. Rolex maintains its leading position, capturing a significant 32% of the total market value. Cartier remains a strong second, solidifying its position within this group.

Performance of Key Players

Richemont's specialty watchmaker division experienced a decline in market share during 2024.

The exclusive “Billionaires’ Club” saw its membership reduced to seven, with Vacheron Constantin falling below the CHF 1 billion sales threshold.

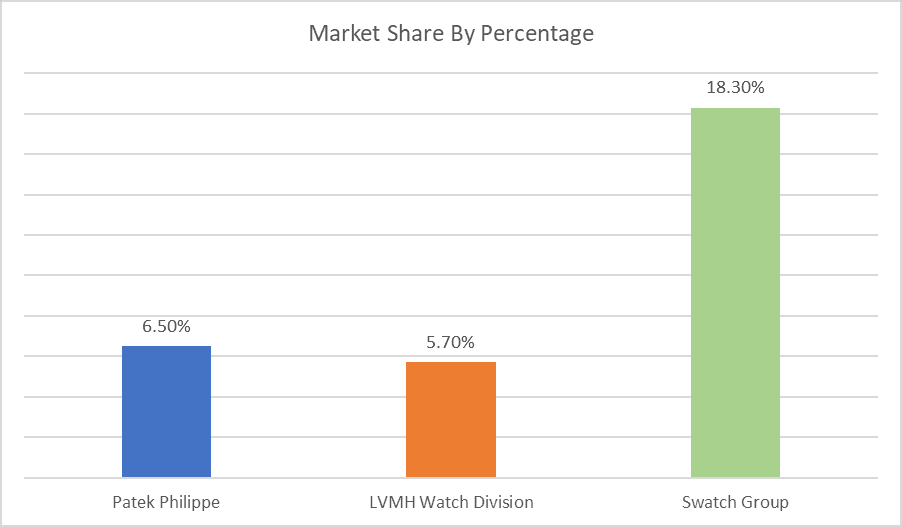

Patek Philippe’s market share (6.5%) now exceeds that of LVMH’s entire watch division (5.7%).

The Swatch Group experienced a notable market share decrease of 200 basis points, settling at 18.3%.

Premiumization Trend Accelerates

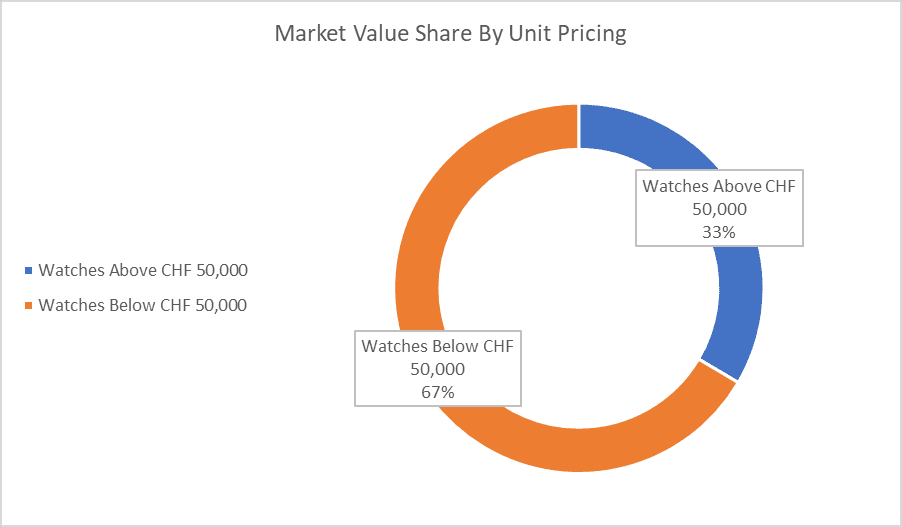

The trend towards premiumization accelerated in 2024. Watches priced above CHF 50,000 now represent 33.5% of the total market value and accounted for an impressive 84% of growth in 2024. This growth occurred despite a 2.8% decline in overall export value, indicating that certain high-price segments managed to thrive.

Market Share Winners

Consistent with previous years, the leading privately owned brands (Rolex, Patek Philippe, Audemars Piguet and Richard Mille) continued to gain market share. This trend distinguishes the Swiss watch sector from the broader luxury goods market, highlighting the unique strength and resilience of these independent players.

Increased Average Unit Price

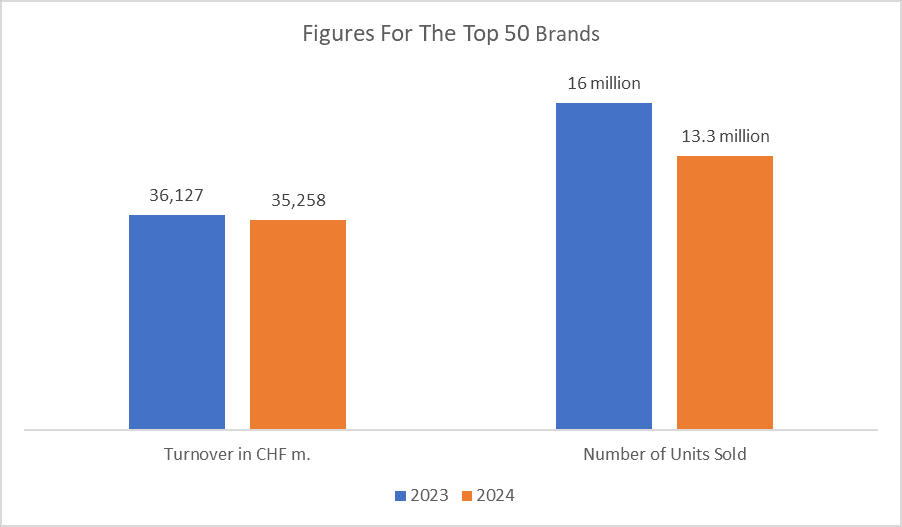

As evident from the report, the upper-end segment of the market is performing better than the mid and entry level segments. Also, the top 50 brands faced turnover contractions as these brands recorded a total turnover of CHF 35,258 billion from their sale of 13.3 million units in 2024 as compared to the turnover of CHF 36,127 billion from sale of almost 16 million units in 2023. These numbers also indicate a significant increase in average price of watches over a period of a year. Overall, only 11 brands out of the top 50 recorded growth in their sales revenues in 2024.

Brand-Specific Performance Analysis

Here’s a chart for the top 20 Swiss watch brands by sales since 2022.

Rank | 2022 | 2023 | 2024 |

1 | Rolex | Rolex | Rolex |

2 | Cartier Watches | Cartier Watches | Cartier Watches |

3 | Omega | Omega | Omega |

4 | Audemars Piguet | Audemars Piguet | Audemars Piguet |

5 | Patek Philippe | Patek Philippe | Patek Philippe |

6 | Longines | Richard Mille | Richard Mille |

7 | Richard Mille | Longines | Longines |

8 | Vacheron Constantin | Vacheron Constantin | Vacheron Constantin |

9 | Breitling | Breitling | Breitling |

10 | IWC | Tissot | Tissot |

11 | Hublot | Swatch | TAG Heuer |

12 | Tissot | IWC | Swatch |

13 | TAG Heuer | Hublot | Hermes |

14 | Jaeger-LeCoultre | Jaeger-LeCoultre | IWC |

15 | Tudor | TAG Heuer | Jaeger-LeCoultre |

16 | Officine Panerai | Hermes | Hublot |

17 | Hermes | Tudor | Bulgari |

18 | Bulgari | Officine Panerai | Officine Panerai |

19 | Blancpain | Bulgari | Chanel |

20 | Chopard | Chopard | Chopard |

Now, let’s look into the detailed analysis of key brand performances, comparing 2024 data with the trends observed from 2021 to 2023.

Rolex Group

Rolex: Despite a slight decrease to 1,176,000 units in 2024 from 1,240,000 in 2023 (following a rise from 1,050,000 in 2021), Rolex maintains its market dominance. This suggests a potential shift towards prioritizing value per watch over sheer volume after a period of rapid expansion.

Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2024 | 10,583 | 1,176,000 | 32% |

2023 | 10,100 | 1,240,000 | 30% |

Tudor: Tudor experienced a continued decline in unit sales, dropping to 160,000 in 2024, a significant 44% decrease. This follows a downward trend from 300,000 units in 2021 to 255,000 in 2023, despite earlier revenue increases.

Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2024 | 360 | 160,000 | 1% |

2023 | 545 | 255,000 | 2% |

Swatch Group

Omega: While maintaining steady sales volume as compared to 2021 - 2023 numbers with increased revenue, Omega saw a decrease to 505,000 units in 2024.

Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2024 | 2,390 | 505,000 | 7% |

2023 | 2,600 | 570,000 | 7% |

Longines: Longines experienced declining sales and revenue from 2021 to 2023. Further impacted by the Chinese market trend in 2024, the brand sold only 950,000 units, a 40% reduction.

Swatch: The brand experienced substantial growth from 3,200,000 units in 2021 to 5,800,000 in 2023, likely driven by the Moonswatch phenomenon. However, sales decreased to 4,900,000 units in 2024.

Breguet: Breguet experienced a decline in both sales and revenue, with sales drastically decreasing from 20,000 to 7,400 watches and revenue dropping significantly from CHF 210 million to CHF 165 million. This decline is worrying for one of the most revered brands under the Swatch umbrella calling for a strong push towards promoting its offerings and attracting mass market appeal for the brand. For the ailing entity, mass-market attention is much needed.

Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2024 | 165 | 7,400 | 1% |

2023 | 210 | 20,000 | 1% |

Glashütte Original: The brand goes from selling 16,000 units in 2023 to just 6,800 in 2024 while maintaining its sales turnover of CHF 55 million. This indicates better performance of its upper-end segment and also increase in average unit prices.

Blancpain: After a slight increase in sales and revenue from 2021-2023, Blancpain's sales dropped to 22,000 units in 2024.

Hamilton: Following increased sales and revenue from 2021-2023, Hamilton sold 118,000 units in 2024.

Tissot: While maintaining sales volume from 2021-2023, Tissot's revenue decreased. 2024 unit sales reached 2,550,000.

Richemont Group

Cartier: Cartier was one of the few brands to increase sales in 2024, reaching 680,000 units.

Vacheron Constantin: Vacheron Constantin's sales decreased to 31,000 units in 2024 from 35,000 in 2023. Notably, the brand is no longer a member of the exclusive “Billionaires’ Club” as it fell below the CHF 1 billion sales threshold.

Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2024 | 942 | 31,000 | 3% |

2023 | 10,100 | 35,000 | 3% |

IWC: IWC sales declined to 120,000 units in 2024 from 137,000 in 2023.

Jaeger-LeCoultre: Jaeger-LeCoultre reported sales of 79,000 units in 2024 compared to 97,000 in 2023.

Van Cleef & Arpels: Despite revenue decreasing from CHF 410 million in 2023 to CHF 296 million in 2024, Van Cleef & Arpels increased its unit sales, which grew from 13,500 to 14,000. The brand gained in market share as well.

Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2024 | 296 | 14,000 | 1% |

2023 | 410 | 13,500 | 1% |

Independent Brands

Audemars Piguet: Audemars Piguet continues its strong growth trajectory, reaching 51,000 units in 2024, bucking the overall market downtrend.

Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2024 | 2,380 | 51,000 | 5% |

2023 | 2,350 | 51,000 | 5% |

Patek Philippe: Patek Philippe, which demonstrated solid performance from 2021 to 2023, increased its sales and revenue, reaching 72,000 units in 2024.

Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2024 | 2,300 | 72,000 | 7% |

2023 | 2,050 | 70,000 | 6% |

Richard Mille: Richard Mille also experienced increased sales compared to 2021 - 2023 numbers, with 5,700 units sold in 2024.

Year | Turnover in CHF m. | Number of Units Sold | Implied Retail Market Share |

2024 | 1,550 | 5,700 | 3% |

2023 | 1,540 | 5,600 | 3% |

F.P. Journe: F.P. Journe, after doubling sales and revenue from 2021 to 2023, sold 1,900 units in 2024.

Breitling: Despite a decrease in units sold, Breitling saw revenue growth from 2021 to 2023. 2024 sales were 160,000 units, mirroring the trend observed in other brands.

Takeaways and Key Observations

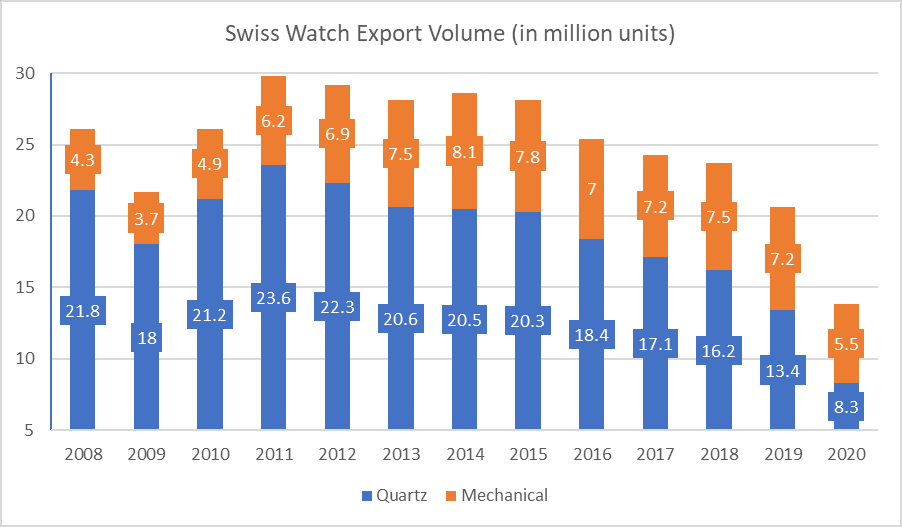

With a better focus on luxury, a clear trend of prioritizing revenue over volume is evident, with many brands implementing price increases to offset stagnant or declining unit sales. The overall watch market has been in decline in terms of volume and thus brands have raised prices to attract desirable revenues. In a broader perspective, the Swiss watch brands exported a total of 29.8 million watches in 2011. In 2020, the number dropped to less than half with only 13.8 million watches exported. For 2024, the number stands at 13,366,560 units sold (approx. 13.3 million). The numbers in terms of volumes are far below that from 2011 and even below the recent high of 2019, wherein the overall unit sales accounted for 20.6 million. Beneath this overall decline is the fact that a lot of Swiss watch brands are actually making more money than they ever did before. In 2017, 7.2 million mechanical watches generated an estimated CHF 15 billion in revenue. Seven years later, 6 million watches generated almost CHF 21 billion in revenue. This indicates that brands have sold more expensive watches. This could either indicate a customer preference shift towards more expensive models or that the models themselves have become more expensive, or actually a mix of both. Either way, the margins are much higher and despite selling fewer watches as an industry, the industry as a whole is doing overall okay.

Also, the continued strong performance of Audemars Piguet, Patek Philippe and Richard Mille highlights the enduring appeal of high-end, independent watchmaking within the current market landscape. While the overall Swiss watch industry is facing a slowdown phase, the market for watches exists in a state of strength and poses an optimistic indicator of the fact that with careful strategizing, growth is certain. The report by Morgan Stanley and LuxeConsult shares a complex narrative for the Swiss watch industry with contrasting attributes for individual brands.